New URAR and UAD 3.6 Appraisal Fees, AMC Tech Fees

February 6, 2026

What’s in This Newsletter (In Order, Scroll Down)

- LIA AD: Using trainees – the safe way

- Will the New URAR and UAD 3.6 Impact Appraisal Fees?

- It looks like an SF apartment complex. It’s actually a $32M estate.

- From Dealerships to AMCs: Tech Fees as the New Normal by Desiree Mehbod

- MY AD: New in the February 2026 issue of Appraisal Today. Book Review: Mein Comp: The Last Appraiser

- “Because Houses Are Human” AI and Appraisers By David Hyman

- Architecture Is About to Grow a Nervous System

- Buildings that are alive

- MBA: Mortgage applications decreased 8.5 percent from one week earlier

Click here to subscribe to our FREE weekly appraiser email newsletter and get the latest appraisal news

———————————————————-

Will the New URAR and UAD 3.6 Impact Appraisal Fees?

Excerpts: With the new URAR and UAD 3.6 rolling out this year, you may be wondering what effect this will have on your fees. While there’s still a lot of uncertainty and speculation around this question, we’re sharing the opinions of professional real estate appraisers who answered our survey, “How do you anticipate the new URAR/UAD 3.6 changes will impact your appraisal fees?”

FEE INCREASES

Over 40% of respondents said they expect their appraisal fees to increase. Still, many respondents (28%) said they anticipate that fees will remain static, and 31% said they are not sure yet. Read their comments below to learn why or why not some appraisers believe their fees will increase with the new URAR and UAD 3.6.

APPRAISER RESPONSES

I Expect Fees to Increase” (41%)

“I have had ample time to practice the new 3.6 through my software and the inspection time will be increasing substantially…. Inspections are going to take some time especially if the dwelling is more than 1,000sf, which most in my market area are well above that. The report cannot be submitted until all sections are 100% complete, so there will be more time contacting agents, homeowners, town facilities, etc. Hoping the learning curve will be quicker than it appears at this point in time.”

I Expect Fees to Stay About the Same” (28%)

FEES REMAIN THE SAME

“I think it will be more labor intensive in the field but easier once you get back to the office.”

“I expect fees to stay the same. There may be less form filling; however, the analysis will remain the same. It’s not about the form or the analytics tools we use; it’s the analysis itself.”

The Bottom Line

While many appraisers anticipate that UAD 3.6 and the new URAR will initially require more time, tighter workflows, and new technology investments, the longer-term outlook is more balanced and, in many ways, promising.

Transitions of this scale often come with short-term growing pains, but clearer data standards, more structured reporting, and modernized tools are designed to create greater consistency and efficiency once the learning curve levels out. As several respondents pointed out, it will take real-world experience to understand where timelines and workloads ultimately settle.

At the same time, the new form offers appraisers a stronger platform to demonstrate the depth of their analysis, judgment, and market expertise.

To read more, Click Here

My comments: THIS IS THE HOTTEST TOPIC IN RESIDENTIAL LENDER APPRAISING. Appraiser opinions are useful but we all want to know what AMCs are planning for fees. I anticipate higher fees by AMCs, borrowers and direct lenders. I have been writing about what is happening since early this year, including details of all the “questions” and uncertainties on the SFR report.

Another significant fee factor is that many appraisers are retiring or quitting because they don’t want to learn the UAD 3.6 for appraisers. Those who stay will have lots of appraisal work as the 11-2-26 mandatory deadline approaches.

UAD 3.6 is not mandatory until November 2, 2026. The Legacy forms will be used during the transition. Will it be done by 11-2-26? Now, software vendors and lenders are way behind. 11-2-27 new mandate date???

On the plus side, 41% of appraisers said fees would go up and are positive about the new reports.

It looks like an SF apartment complex. It’s actually a $32M estate.

Excerpts: A 1905 apartment building at 3199 Jackson St. in SF’s Presidio Heights has been transformed into a 26,000-square-foot private estate now listed for $32 million

According to listing agent Max Armour, 3199 Jackson St. could be easily mistaken for the historic seven-unit building it once was, as the exterior facade has been deliberately maintained to look just as it did over a century ago. But make no mistake: This 26,260-square-foot estate is now owned by one family. The award-winning firm of Butler Armsden Architects transformed the apartment building into a luxurious compound, a process of reconstruction and renovation that took 10 years. The overhaul is complemented by the work of internationally lauded interior designer Jonathan Rachman.

To read more, Click Here

My comments: Highest and best use is a mansion, not an apartment? Thanks to Joe Lynch for this interesting listing!

——————————————————————–

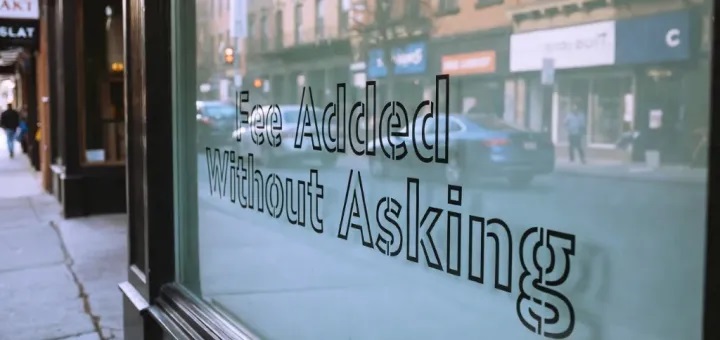

From Dealerships to AMCs: Tech Fees as the New Normal

by Desiree Mehbod

Excerpts:

Tech fees have spread so far and wide that even my oil change felt like a crash course in AMC logic.

Last year I went to the dealership for a simple oil change. Nothing dramatic. I was prepared to drink bad waiting room coffee, scroll my phone, and leave. Instead, the service rep came out with the classic “while we had it up on the lift” routine and told me I needed new brakes. Fine. I approved the $1,200 estimate. Not fun, but expected. When the work was done, I went to pay and noticed a mysterious $60 surcharge added to the invoice. I asked what it was, and the cashier said it was a credit card fee, a five percent add‑on for using the most common form of payment on earth. I told her to call the service rep because I wasn’t accepting a surprise fee at the finish line. He explained that if I paid cash or wrote a check, the fee would be removed.

Chase Pursley recently asked on LinkedIn why appraisers tolerate portal fees and what other industry gets to pass its cost of doing business down as a line item. Appraisers chimed in with everything from frustration to fatalism. One said fighting tech fees is like changing the radio station while driving toward a cliff. Another said they have never understood how AMCs justify passing their operating costs to the appraiser, especially when AMCs are acting as the lender’s agent.

And here is the part that makes AMC tech fees even more absurd than the dealership’s credit card surcharge: at least the dealership was charging its own customer. AMCs are charging appraisers, who are not their customers at all. Borrowers pay for the appraisal. Lenders hire the AMC. Yet somehow the AMC’s cost of doing business gets pushed onto the only party who isn’t their customer but is still required to use their system if they want the work.

To read more and 40+ appraiser comments, Click Here

My comments: Nothing new. Quit working for AMCs. There are other options. Will AMCs increase what they pay for UAD 3.6 appraisals???

—————————————————————-

Are you getting too many ad-only emails?

4 ways to get only the FREE email newsletters and NOT the ad-only emails.

1. Twitter: https://twitter.com/appraisaltoday Posted by noon Friday

2. Read on blog www.appraisaltoday.com/blog Posted by noon Friday. You can subscribe to the blog in the upper right of each blog page. NOTE: the popular ads with liability tips are below the first topic on my blog posts.

3. Email Archives: https://appraisaltoday.com/archives

(posted by noon Friday) The link is above and to the left of the big yellow email signup form. Newsletters start with “Newz.” Contains all recent emails sent.

4. Link to the 10 most recent newsletters (no ads) at www.appraisaltoday.com. Scroll down past the big yellow signup block. The newsletters have abbreviated titles, taken from their blog posts.

To read more about the 4 ways, plus information on why I take ads, etc.

—————————————————————————

New in the February 2026 issue of Appraisal Today

- Mein Comp: The Last Appraiser, Book Reviewed by Ann O’Rourke, SRA, MAI

- Review of Mein Comp, Reviewed by Jeremy Bagott, MAI

- The Cost Approach for Appraisers is not popular, by Tim Andersen, MAI

- Chapter 1 of Mein Comp, the Last Appraiser

Mein Comp, the Last Appraiser It is the best appraisal book I have ever read. When I started reading the book I could not put down for many hours, took a break and finished the book!

9 Chapters tell the history of what caused “the Last Appraiser” from 2009 (AMCs) through 12-31-29

————————-

The Cost Approach

“We use the Cost Approach because it helps us to analyze markets, recognize trends, and credibly appraise real property.

Once again, Tim Andersen took on an unpopular appraisal topic. I had never heard before the concepts and techniques he discusses. I had mostly used it for new construction to see if it was feasible.

To read the articles, plus 3+ years of previous issues, subscribe to the paid Appraisal Today at www.appraisaltoday.com/order

Not sure if you want to subscribe?

Sign up for monthly auto renewal for $8.25!

Cancel at any time for any reason! You will receive a prorated refund.

$8.25 per month, $24.75 per quarter, and $89 per year (Best Buy)

or $99 per year or $169 for two years

Subscribers get FREE: past 18+ months of past newsletters

What’s the difference between the Appraisal Today free Weekly email newsletter and the paid Monthly newsletter? Click here for more info.

If you are a paid subscriber and did not receive the

February, 2026 issue emailed on

Monday February 2, 2026 please email info@appraisaltoday.com, and we will send it to you. You can also hit the reply button. Be sure to include a comment requesting it. Or, call 510-865-8041

—————————————————-

“Because Houses Are Human”

AI and Appraisers

By David Hyman

Excerpts:

What’s in Your Tool Belt?

Artificial Intelligence can be the new calculator (or Abacus), the new measuring tape or wheel, or even better, the new, extra you. Appraising real estate at the residential level is all about experienced learning. It doesn’t matter if you are great writer, a terrific architect, or the best-selling realtor in the city. It takes refinement to get good. And to get great, well, that takes commitment too.

The truth about AI in the realm of fee appraisal, is that it can be intimidating if you are not confident in your abilities, or if you have limited experience in the field. Those people that seem to get where they want to be in life always embrace change and see opportunity.

If you look at AI as an opportunity, you will have the chance to define it for your business and perhaps for the profession. For me, AI is the most exciting development in the world of appraisal since the invention of the digital camera. It is like having an assistant that is better at math than the ladies in the NASA movie, Hidden Figures.

To read more, Click Here

My comments: Interesting use of ChatGPT. Worth reading about one appraiser’s use of AI and his opinions of AI for appraisers.

—————————————————

Architecture Is About to Grow a Nervous System

Buildings that are alive

Buildings that sense, heal, and evolve aren’t science fiction—they’re being cultivated in labs right now.

Excerpts: The interest in commercializing living systems in products and buildings has inspired a new category of material technology called Engineered Living Materials (ELMs).

The notion of living architectural materials was once a fantasy. The emergence of responsive systems such as microalgae facades demonstrated the possibilities of living-organism-supported building applications—albeit experimental ones. The interest in commercializing living systems in products and buildings has inspired a new category of material technology called Engineered Living Materials (ELMs).

These biologically based substances enable capacities such as environmental responsiveness, self-repair, and growth—behaviors that conventional products lack. The significance is profound: ELMs bridge the gap between biology and construction, redefining building materials as dynamic and evolving participants in the constructed environment.

To read more, Click Here

My comments: AI is not much in comparison with this!! I don’t get to use my B.S. in Biology often. Finally it is applied to buildings that are alive…. Many thanks again to Joe Lynch for this fascinating link!

—————————————————————-HOW TO USE THE NUMBERS BELOW. Appraisals are ordered after the loan application. These numbers tell you the future for the next few weeks. For more information on how they are compiled, Click Here.

Note: I publish a graph of this data every month in my paid monthly newsletter, Appraisal Today. For more information or get a FREE sample go to www.appraisaltoday.com/order Or call 510-865-8041, MTW, 7 AM to noon, Pacific time.

My comments: Rates are going up and down. We are all waiting for rates to drop lower in 2026.

Mortgage applications decreased 8.5 percent from one week earlier

WASHINGTON, D.C. (January 28, 2026) — Mortgage applications decreased 8.5 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending January 23, 2026. This week’s results include an adjustment for the Martin Luther King Jr. Day federal holiday.

The Market Composite Index, a measure of mortgage loan application volume, decreased 8.5 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 16 percent compared with the previous week. The Refinance Index decreased 16 percent from the previous week and was 156 percent higher than the same week one year ago. The seasonally adjusted Purchase Index decreased 0.4 percent from one week earlier. The unadjusted Purchase Index decreased 4 percent compared with the previous week and was 18 percent higher than the same week one year ago.

“Mortgage rates increased for the first time in a month, and as expected, refinance applications fell by 16 percent. The 30-year fixed rate was the highest in three weeks at 6.24 percent,” said MBA’s Joel Kan, Vice President and Deputy Chief Economist. “FHA refinance activity bucked the overall trend and increased, as FHA rates remained almost 20 basis points lower than conforming rates. With rates holding in the 6 percent range, the refinance market is likely to remain sensitive to week-to-week rate movements.”

Added Kan, “Purchase applications were 18 percent higher than last year’s pace, and the average loan size stayed at its highest level since September 2025, signaling that prospective homebuyers remain active at the start of 2026.”

The refinance share of mortgage activity decreased to 56.2 percent of total applications from 61.9 percent the previous week. The adjustable-rate mortgage (ARM) share of activity increased to 7.6 percent of total applications.

The FHA share of total applications increased to 18.6 percent from 15.9 percent the week prior. The VA share of total applications decreased to 14.7 percent from 16.2 percent the week prior. The USDA share of total applications increased to 0.5 percent from 0.4 percent the week prior.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($832,750 or less) increased to 6.24 percent from 6.16 percent, with points increasing to 0.55 from 0.54 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans. The effective rate increased from last week.

The average contract interest rate for 30-year fixed-rate mortgages with jumbo loan balances (greater than $832,750) decreased to 6.34 percent from 6.39 percent, with points increasing to 0.40 from 0.38 (including the origination fee) for 80 percent LTV loans. The effective rate decreased from last week.

The average contract interest rate for 30-year fixed-rate mortgages backed by the FHA increased to 6.06 percent from 6.04 percent, with points increasing to 0.75 from 0.73 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The average contract interest rate for 15-year fixed-rate mortgages increased to 5.64 percent from 5.55 percent, with points decreasing to 0.61 from 0.65 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The average contract interest rate for 5/1 ARMs increased to 5.56 percent from 5.42 percent, with points increasing to 0.80 from 0.62 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The survey covers U.S. closed-end residential mortgage applications originated through retail and consumer direct channels. The survey has been conducted weekly since 1990. Respondents include mortgage bankers, commercial banks, thrifts, and credit unions. Base period and value for all indexes is March 16, 1990=100.

———————————————-

Ann O’Rourke, MAI, SRA, MBA

Ann O’Rourke, MAI, SRA, MBA

Appraiser and Publisher Appraisal Today

1826 Clement Ave. Suite 203 Alameda, CA 94501

Phone: 510-865-8041

Email: ann@appraisaltoday.com

Online: www.appraisaltoday.com

We want to know what you think!! Please leave a comment.