Newz: Ready for UAD 3.6?, ADU Growth, Future of Data Collection

August 7, 2026

What’s in This Newsletter (In Order, Scroll Down)

- LIA AD: Subpoena Threat Over a 10-Year-Old Appraisal

- UAD 3.6 Is Here. Are You Ready? By Scott Reuter, Freddie Mac

- New Cantilevered Home for $45,000,000 in Park City Utah

- Property Valuation and the Future of Data Collection

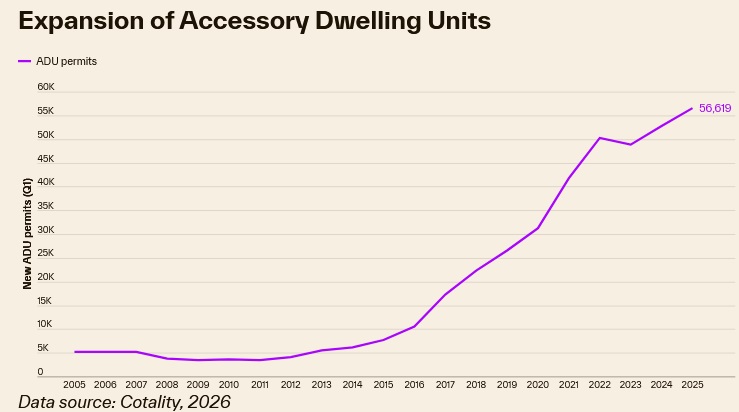

- Explosive ADU growth By Ryan Lundquist

- The Full Measure: July 2026 Economic Outlook By Kevin Hecht, SRA

- My UAD 3.6 Tips of the week.

- MBA STATS: Mortgage applications decreased 6.4 percent from one week earlier

UAD 3.6 Is Here. Are You Ready?

Q&A with Scott Reuter, Chief Appraiser at Freddie Mac

Excerpts: AB: Are there additional impacts of the new report structure that should help the appraiser?

Reuter: Yes, one such change is in how defects, damages, and deficiencies are reported. For the subject property (structure, site, and any outbuildings), the appraiser will identify what they observed and where it’s located. They can provide a description of the issue and photos in a dedicated section of the report. Again, no more searching for this information in the addenda. This will bring more clarity around damage, defects, and deficiencies and should result in fewer revision requests.

AB: You’ve discussed some benefits to appraisers, but are there things they need to consider with UAD 3.6 too?

Reuter: With increased transparency comes a greater emphasis on accountability. Appraisers are encouraged to clearly outline what was done and demonstrate their methods. For example, it will become more important to accurately indicate who contributed significant appraisal assistance or who inspected the property. The new standard will provide clearer guidance on reporting these details.

Furthermore, the updated standard places additional focus on market analysis and the rationale behind market condition adjustments. Since market analysis forms the foundation of an appraisal, UAD 3.6 encourages appraisers to not only perform thorough analyses but also to document their process, rather than simply entering numbers into the form. Many appraisers already excel in this area, and others may find it helpful to provide supporting evidence for how market condition adjustments — those of $0 — are determined. This approach aims to foster more reliable and credible results, ultimately enhancing the quality of appraisals.

To read more, Click Here

My comments: Worth reading all the Q and A’s. Well written and understandable by an Expert – Scott Reuter, Chief Appraiser at Freddie Mac

——————————————————————

New Cantilevered Home for $45,000,000 in Park City Utah

Excerpts: 6 bedrooms,

9.5+ baths, 13,2779 sq.ft., 1.89 acre lot, built in 2026

Mount Rushmore and mountain panoramas: The Vandamm House seen in Alfred Hitchcock’s spy thriller “North by Northwest” features a cantilevered, Frank Lloyd Wright-inspired design set on a ridgeline.

Nestled in the exclusive Promontory Club, the midcentury mansion boasts a “40-foot cantilever projecting the glass-walled great room” that opens up to unobstructed valley views. Architectural details found throughout the 13,279-square-foot open floor plan include glass walls, custom walnut cabinetry, cork wallpaper, an elevator, and “lovingly restored original” furnishings and artwork. Lavish amenities include three kitchens, six en suite bedrooms prewired for a supplemental oxygen system, an 18-seat home theater with “constellation ceiling,” a half-circle wet bar that opens up to a pool terrace, and a wellness wing with steam, an infrared sauna, and a gym.

The 1.89-acre property also has a pool and 50-vehicle auto showroom with a commercial ventilation system, storage area, detailing bay, and electric charging stations.

To read the listing with many photos, Click Here

To see 5 Cantilevered homes, including this one, Click Here

My comments: I love cantilevered homes, especially next to an ocean. I have no idea why!

——————————————————————–

Property Valuation and the Future of Data Collection

Excerpts: Property data collection has quietly become one of the most consequential shifts in modern real estate, reshaping how lenders, AMCs and national platforms gather the information that ultimately determines a homeowner’s equity, a buyer’s loan terms and the integrity of the appraisal process itself. Yet most consumers have no idea who is actually walking through their home, measuring rooms, photographing conditions or documenting features. In many states, the answer is startling: no license, no training requirement, no background check, no oversight, and no accountability. RealEstate

The Virginia Real Estate Appraiser Board’s Emerging Industry Issues Committee is taking a hard look at this rapidly expanding practice, and for the first time, is asking appraisers, regulators, realtors, homeowners, lenders and anyone with a stake in property valuation to weigh in. The Board has launched a statewide survey, Property Data Collectors: A Survey of Regulatory Agencies and the Appraiser Industry, to gather real world experiences, concerns, risks and recommendations as it evaluates whether property data collectors should be regulated or licensed in Virginia.

To take the survey, Click Here

This is not just an appraisal issue. It is a consumer protection issue, a real estate industry issue, and a community issue. Anyone who owns a home, plans to buy one, works in real estate, or simply cares about the integrity of property valuation has a stake in how Virginia approaches this question. The data collected today will shape tomorrow’s regulatory framework, whether that means licensure, registration, employer oversight or something entirely new.

Your voice matters here. Whether you have encountered property data collectors firsthand, have concerns about consumer safety, believe they should be trained and regulated, or simply want transparency in who enters a home during the mortgage process, the Board wants to hear from you. This is your chance to influence policy before decisions are made.

Take the survey, share it with colleagues, send it to friends and neighbors, and help Virginia build a regulatory approach that protects consumers, supports appraisers and strengthens trust in the valuation process.

To read more, Click Here

My comments: I took the survey. Worth reading the details including appraiser comments. UAD 3.6 Data Collection with a data collector formerly working at Walmart??

——————————————————————–

Are you getting too many ad-only emails?

4 ways to get only the FREE email newsletters and NOT the ad-only emails.

1. Twitter: https://twitter.com/appraisaltoday Posted by noon Friday

2. Read on blog www.appraisaltoday.com/blog Posted by noon Friday. You can subscribe to the blog in the upper right of each blog page. NOTE: the popular ads with liability tips are below the first topic on my blog posts.

3. Email Archives: https://appraisaltoday.com/archives

(posted by noon Friday) The link is above and to the left of the big yellow email signup form. Newsletters start with “Newz.” Contains all recent emails sent.

4. Link to the 10 most recent newsletters (no ads) at www.appraisaltoday.com. Scroll down past the big yellow signup block. The newsletters have abbreviated titles, taken from their blog posts.

To read more about the 4 ways, plus information on why I take ads, etc.

Click here

—————————————————————–

UAD CLASSES

In the August 26, 2026 issue of Appraisal Today

Excerpts: Your software provider probably has classes on their software, which includes details on how to complete the report, such as Access to Broadband. FYIGSEs are planning on including such as Starlink to broadband.

Most appraisers have only taken the GSE class which is good but you will need a lot more classes and software training.

There are many webinars, but I primarily focus on classes, especially with CE.

Companies with lists of classes and links for more information: Appraiser eLearning, McKissock and Appraisal Institute.

All offer the Fannie Class, so I did not include details.

I did not include other CE companies as most only offered the Fannie class above. They may have webinars.

Only McKissock offers a certification, which may be helpful when getting clients.

===========================================

To read the full article, plus 3+ years of previous issues, subscribe to the paid Appraisal Today at www.appraisaltoday.com/order .

Not sure if you want to subscribe?

Sign up for monthly auto renewal for $8.25!

Cancel at any time for any reason! You will receive a prorated refund.

$8.25 per month, $24.75 per quarter, and $89 per year (Best Buy)

or $99 per year or $169 for two years

Subscribers get FREE: past 18+ months of past newsletters

What’s the difference between the Appraisal Today free Weekly email newsletter and the paid Monthly newsletter? Click here for more info.

Explosive ADU growth & going viral online

By Ryan Lundquist

Excerpts: Some new research from Cotality shows an explosion of ADU permits in the United States, so we have a real trend on our hands. However, I’d like to see how much California means here in the data since California had 72% of the ADU permits in the country in 2025 according to Cotality research.

The line between an ADU and a full-fledged second unit is getting blurry. For instance, last week someone asked me if a duplex with an ADU would be considered a triplex. That’s a good question. Let me ask you this. Is a single-family home with an ADU a duplex? I’m not trying to create confusion. All I’m saying is there are some big questions ahead, and expect a growth curve for the real estate community and lenders. I believe lenders have been behind the ball already with not allowing an ADU on a duplex, but thankfully this is changing (thanks Joe for the comment (I updated this sentence))

MLS added an “ADU” field a couple years ago, and this is a great feature that many people don’t know about. Check out how many properties come up with potential ADUs when I’m looking at current listings, pendings, and sales in 2026. If you don’t see the “ADU” field while doing a map search, click “fields’, and then add the “ADU/2nd Unit” category so it will show up during every search from now on. You can also try the “Other Structures” field and then select “Guest House” to see if that works. I find when searching for ADUs, we have to try different ways of finding comps. In addition to these two fields, I would also click “search criteria” and “public remarks” to type in stuff like, “ADU,” “mother-in-law,” and “guest quarters.”

To read more, Click Here

My comments: Good article on ADUs, especially the tips on how to find them on MLS! Worth reading. See which states have the most ADUs and more info.

——————————————————————-

The Full Measure: July 2026 Economic Outlook

By Kevin Hecht, SRA

Excerpts: Welcome to the July 2026 edition of The Full Measure. Each month, we step back from our daily appraisal assignments, set down the tape measures, and examine the broader economic landscape to understand the “why” behind the market data we analyze daily.

We are the boots on the ground, witnessing firsthand how national policies, global events, and economic shifts translate into local property values.

This month, the data tells a story of a market caught between two competing forces: an economy that continues to grow faster than most expected, and a housing sector that remains in what RBC Economics aptly calls “a deep freeze.”

Understanding both sides of that tension is essential to producing credible appraisal reports in the months ahead.

The Appraiser’s Role: The Macro Stabilizer

As appraisers, the July data reinforces several practical realities that should inform our work right now.

First, the gap between list price and sale price is widening in many markets as sellers recalibrate to the affordability ceiling. Carefully analyzing final sale prices, not list prices, and scrutinizing seller concessions is more important than ever.

Concessions that buy down a buyer’s mortgage rate are now common enough in many markets to require explicit consideration in our comparable sales analysis.

Second, the divergence between the new-home and existing-home markets is a meaningful valuation variable. Builders are offering incentives that effectively reduce the true cost of a new home below its contract price.

When new construction is a relevant market segment in your assignment, the impact of those concessions on market value must be addressed.

Third, the upcoming Q2 GDP report, the June PCE inflation data, and the FOMC announcement all arrive in the week of July 28th. That is an unusually dense calendar of market-moving data. Appraisers with assignments that close in August should be prepared for potential volatility in mortgage rates and buyer sentiment as the market digests those releases.

Our role as the Macro Stabilizer in the real estate finance ecosystem has never been more important. We do not make the market. We measure it, and in measuring it accurately, we help keep it honest.

Until next time, stay diligent, stay curious, and keep measuring the market.

To read more, Click Here

My comments: Written by an appraiser and economist.The article has a table of economic factors. Worth checking out, plus other topics. The only economics article that discusses what it means for appraisers. The only economics article I read. Anyone can understand this article.

I had to take an economics class to get my MBA. I am not a big fan of economics – a bit technical in classes. But, it is one of the basic classes for understanding real estate appraisal.

I got my MBA in 1980, 5 years after I started appraising. I had never taken any business classes (Degree in Biology). I needed to learn more, so I got an MBA. I am a better appraiser. Much easier than getting a 4 year business degree!

——————————————————————–

WEEKLY UAD 3.6 TIPS

The November 2 deadline will NOT be changed (What GSEs say.) I agree.

My opinion of UAD 3.6. If I was doing GSE appraisals I would learn how to use the software I select. Far superior to forms, which require a large comments section. In UAD 3.6 Photos are next to the comps and located next to what you are describing about the subject. UAD 3.6 is much more understandable for borrowers than forms with the strange codes and limited space inside the form and more….

Read the first article above in this newsletter for details on how to get ready.

When you are ready to do UAD 3.6 appraisals, contact AMCs chief appraisers and your contacts at lenders and ask to have this put into your profile, so you will more easily get on their lists for appraisers available to do UAD 3.6 appraisals.

You will be on the top of the list!!

———————————————————————

HOW TO USE THE NUMBERS BELOW. Appraisals are ordered after the loan application. These numbers tell you the future for the next few weeks. For more information on how they are compiled, Click Here.

Note: I publish a graph of this data every month in my paid monthly newsletter, Appraisal Today. For more information or get a FREE sample go to www.appraisaltoday.com/order Or call 510-865-8041, MTW, 7 AM to noon, Pacific time.

My comments: Rates are going up and down. We are all waiting for rates to drop lower in 2027.

Mortgage applications decreased 6.4 percent from one week earlier

WASHINGTON, D.C. (July 29, 2026) — Mortgage applications decreased 6.4 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending July 24, 2026.

The Market Composite Index, a measure of mortgage loan application volume, decreased 6.4 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 6 percent compared with the previous week. The Refinance Index decreased 10 percent from the previous week and was 2 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 4 percent from one week earlier. The unadjusted Purchase Index decreased 3 percent compared with the previous week and was 3 percent higher than the same week one year ago.

“Following last week’s spike in oil prices, mortgage rates moved higher, with the 30-year fixed rate increasing to 6.76 percent, the highest rate since August 2025,” said Joel Kan, CMB, MBA’s Vice President and Deputy Chief Economist. “This upward trajectory in rates continues to significantly impact refinance borrowers, with a 10 percent decline in refinance applications, including a steeper drop in government refinances. Despite housing inventory increasing in certain markets, higher rates have added to ongoing affordability challenges for many homebuyers, which drove the decrease in purchase activity over the week.”

The refinance share of mortgage activity decreased to 39.5 percent of total applications from 41.2 percent the previous week. The adjustable-rate mortgage (ARM) share of activity increased to 8.1 percent of total applications.

The FHA share of total applications decreased to 16.9 percent from 17.0 percent the week prior. The VA share of total applications decreased to 12.6 percent from 13.2 percent the week prior. The USDA share of total applications decreased to 0.4 percent from 0.5 percent the week prior.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($832,750 or less) increased to 6.76 percent from 6.69 percent, with points increasing to 0.69 from 0.62 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans. The effective rate increased from last week.

The average contract interest rate for 30-year fixed-rate mortgages with jumbo loan balances (greater than $832,750) increased to 6.70 percent from 6.44 percent, with points increasing to 0.52 from 0.45 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The average contract interest rate for 30-year fixed-rate mortgages backed by the FHA increased to 6.41 percent from 6.34 percent, with points increasing to 0.88 from 0.74 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The average contract interest rate for 15-year fixed-rate mortgages increased to 6.15 percent from 6.04 percent, with points decreasing to 0.84 from 0.87 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The average contract interest rate for 5/1 ARMs increased to 5.98 percent from 5.97 percent, with points increasing to 1.23 from 1.11 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The survey covers U.S. closed-end residential mortgage applications originated through retail and consumer direct channels. The survey has been conducted weekly since 1990. Respondents include mortgage bankers, commercial banks, thrifts, and credit unions. Base period and value for all indexes is March 16, 1990=100.

——————————————

Ann O’Rourke, MAI, SRA, MBA

Appraiser and Publisher Appraisal Today

1826 Clement Ave. Suite 203 Alameda, CA 94501

Phone: 510-865-8041

Posted in:

Uncategorized