Newz: 24 Hour Appraisal, Disclose When Some One Else Did the Inspection

November 7, 2025

What’s in This Newsletter (In Order, Scroll Down)

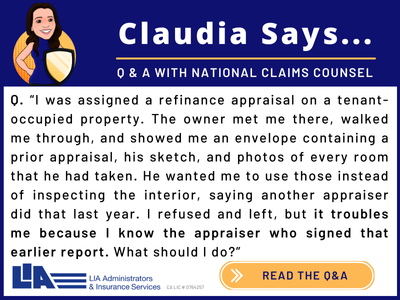

- LIA AD: When a Property Owner Wants to Do the Appraiser’s Job

- The Hazards of Signing a URAR When Another Person Conducts the Inspection

- Honolulu Diamond Head Estate for $34,000,000

- The 24-Hour Appraisal Funded by Appraisers

- How Policy, Data, and Technology Are Reshaping Lending and Valuation: MBA 2025 Recap

- MBA: Mortgage applications decreased 1.9 percent from one week earlier

———————————————————————–

Click here to subscribe to our FREE weekly appraiser email newsletter and get the latest appraisal news

———————————————–

———————————————-

The Hazards of Signing a URAR When Another Person Conducts the Inspection

By Dan Bradley

Excerpts: When using the Uniform Residential Appraisal Report (URAR) to report the results of an appraisal, the appraiser’s signature on the report is not merely a formality, it is a certification. By affixing his or her signature, the appraiser is certifying to (among other things) having personally made an interior and exterior inspection of the subject property.

Clients, AMCs, and state regulatory agencies are reporting that appraisers are increasingly delegating their inspection responsibilities to others yet are signing the URAR certifying they made a personal inspection.

What are the risks if an appraiser signs a URAR report certifying an interior and exterior inspection that was actually conducted by someone else?

Conclusion

Signing a URAR appraisal report that states the appraiser personally inspected the property, when in fact another party performed the inspection, is a serious liability risk. USPAP permits an appraiser to value a property that they did not make an interior and exterior inspection.

However, USPAP does not allow an appraiser to communicate a misleading report. A report that falsely indicates that an individual made an inspection of a property when in fact they did not is misleading, and could result in disciplinary action, civil liability, or other negative consequences.

To read more, Click Here

My comments: Good reminder, especially with the use by the GSEs of alternative valuation methods. Of course, you know nothing about the qualifications of the person doing the inspection. The article did not specifically address UAD 3.6, but I assume it would have the same certification section and requirements.

———————————————————————

Honolulu Diamond Head Estate for $34,000,000

Excerpts: 4 bedroom, 4.5 baths, 5,226 sq.ft., 34,157 sq.ft. lot, built in 19741

Lovingly maintained and meticulously upgraded, showcases an extraordinary level of craftsmanship, preservation, and pride. Honoring the property’s architectural heritage while introducing modern enhancements that elevate daily living.

From the custom woodwork, curated interiors, and peaceful lanais, every element exudes quality and intention.

Central to the plan of the garden, which was meant to create “an oasis in the midst of chaos”, were water features and arbors, which bring shade and structure to the garden with the addition of terraces connected by a winding path. The fountains and water features add visual beauty to the garden, as well.

Tucked into the side of one of the lower hillside terraces, the path wanders up to and around a small yoga studio and guest cottage.

To read the listing plus a video, 25 photos and more, Click Here

——————————————————————-

The 24-Hour Appraisal Funded by Appraisers

Excerpts: The 24-hour appraisal model runs on borrowed time and borrowed credibility. Guess who’s underwriting both.

Reggora’s “24-hour appraisal” pitch was flimsy from the start, and now that we’ve seen the fine print, it’s not innovation, it’s a liability handoff wrapped in buzzwords. Their shiny new “Streamlined Appraisal” is just another hybrid, bifurcated product dressed up to look like progress. And like most hybrids, it assumes appraisers are either desperate, asleep, or willing to sign off on someone else’s work for peanuts.

Brian Zitin proudly explains that Reggora sends a property data collector to the home before the borrower even commits to the loan. They gather the Uniform Property Data Set, and get this, don’t charge the lender or borrower for it, even if the deal falls through. Sounds generous, until you realize someone has to eat that cost. Spoiler, it’s not the lender, and it’s definitely not Reggora.

A peer recently forwarded an FHA appraisal order from Appraisal Marketplace, Reggora’s AMC, offering a fee of $280. That’s not a typo. In 2025, they’re offering less than what appraisers earned in the early ’90s. And this isn’t just a random lowball, it’s the business model. Reggora pays property data collectors upfront, even when loans fall apart, then recoups the loss by slashing appraiser fees to bargain bin levels. The screenshot, with identifying info blurred, is a perfect snapshot of this ‘revolution.’ Same AMC tactics, now with a tech halo and a stopwatch.

To read more, plus the 40+ appraiser comments Click Here

My comments: I had always been a bit suspicious of Regorra’s 24 hour turn time. See the link above for disclosing that you did not do the inspection.

—————————————————————-

Are you getting too many ad-only emails?

4 ways to get only the FREE email newsletters and NOT the ad-only emails.

1. Twitter: https://twitter.com/appraisaltoday Posted by noon Friday

2. Read on blog www.appraisaltoday.com/blog Posted by noon Friday. You can subscribe to the blog in the upper right of each blog page. NOTE: the popular ads with liability tips are below the first topic on my blog posts.

3. Email Archives: https://appraisaltoday.com/archives

(posted by noon Friday) The link is above and to the left of the big yellow email signup form. Newsletters start with “Newz.” Contains all recent emails sent.

4. Link to the 10 most recent newsletters (no ads) at www.appraisaltoday.com. Scroll down past the big yellow signup block. The newsletters have abbreviated titles, taken from their blog posts.

To read more about the 4 ways, plus information on why I take ads, etc.

—————————————————

UAD 3.6 Update – Software Vendors, Both Old and New and More Info

In the August 2025 issue of Appraisal Today

Excerpts: In October, none of the software vendors were ready to use software for completing appraisals. They are focusing on the Broad Production start date of January 26, 2026, but I don’t know who will complete the software by that date. A few months ago, I had live demos where I asked questions, from a la mode, Bradford and SFREP and wrote an article about them.

Recently appraiser Andy Arledge, who developed Appraiser Genie Software. He now has Freedom Appraise software for UAD 3.6,.

There are at least 3 new software companies with Venture Capital funding.

The appear to use much more AI. I will be getting live demos on these software companies.

Three Major Factors to be completed before the software is usable.

1. UAD 3.6 software – “PDF Report” with Fannie Validation completed.

2. Integration of “add ons” such as vendor’s software and Spark, Datamaster, etc.

3. New mobile app. In my opinion, this is mandatory for any appraiser wanting to

do UAD 3.6 reports.

What about AMCs and fees – THE TOP QUESTION?

Everyone is worried about AMC fees of $350 or lower. No one knows what will

happen.

I answer many more questions in this article.

To read the full article, plus 5 more articles on UAD 3.6, and 2+ years of previous issues, subscribe to the paid Appraisal Today.

Not sure if you want to subscribe?

Sign up for monthly auto renewal for $8.25!

Cancel at any time for any reason! You will receive a prorated refund.

$8.25 per month, $24.75 per quarter, and $89 per year (Best Buy)

or $99 per year or $169 for two years

Subscribers get FREE: past 18+ months of past newsletters

What’s the difference between the Appraisal Today free Weekly email newsletter and the paid Monthly newsletter? Click here for more info.

————————————————————-

If you are a paid subscriber and did not receive the November, 2025 issue emailed on Monday, November 3 , 2025 please email info@appraisaltoday.com, and we will send it to you. You can also hit the reply button. Be sure to include a comment requesting it. Or, call 510-854-8041

——————————————————————–

How Policy, Data, and Technology Are Reshaping Lending and Valuation: MBA 2025 Recap

Excerpts: The Mortgage Bankers Association Annual Conference is always one of the best places to figure out what is coming for the industry for the coming year. Instead of the usual mix of uncertainty and cautious hope, there was a steady drumbeat of progress from Washington, thoughtful debate about the economy, and a very practical focus on how work is changing inside lending and valuation.

If you are a lender or an appraiser, the message was clear. You need to start taking on the changes in the industry now. The day to day tools of our jobs are being rebuilt around structured data and responsible uses of artificial intelligence.

If you boil the week down to one line, it is this. There is a lot of change coming for the industry, the economy is steady with some real risks, and the core workflows in lending and valuation are being rebuilt around structured data, transparent reports, and responsible automation. The winners will be the teams that prepare early, explain the changes clearly to everyone involved, and keep the human relationship at the center of the process.

To read more, Click Here

My comments: Written for appraisers. Few appraisers attend MBA conferences. If you do lender appraisals, it is important to see what the Mortgage Bankers say.

If you are a lender or an appraiser, the message was clear. You need to start taking on the changes in the industry now. The day to day tools of our jobs are being rebuilt around structured data and responsible uses of artificial intelligence.

This article was written for appraisers.

—————————————————————–

October 2025 Housing Market Updates for Appraisers

By Kevin Hecht, Appraiser and Economist

Excerpts: The housing market in October 2025 presents a paradox: falling mortgage rates and renewed buyer activity suggest recovery, yet a federal government shutdown, persistent affordability challenges, and shifting regional dynamics reveal a market in transition.

The fourth quarter opens with cautious momentum tempered by significant headwinds.

For real estate appraisers, these conditions demand heightened analytical rigor, sophisticated time adjustment analysis, and a deep understanding of local market variations.

- Fed Cuts Again, But Signals Caution Ahead

- Downstream Effects of the Government Shutdown

- Fed Caution: Limited Mortgage Relief

- Buyers Return, But Is It Sustainable?

- Appreciation Trend Breaks: Prioritize Recent Comps Amid Sub‑Market Divergence and Rate Uncertainty

- Government Shutdown: An Underappreciated Disruption

- Government-Backed Loan Uncertainty Narrows Buyer Pool, Slows Market, Complicates Valuations

- Regional Disparities: National Trends Are Increasingly Irrelevant

- Credibility Requires Local Market Mastery, Not National Statistics

- The All-Cash Buyer Phenomenon: A Fundamental Shift

- Final Takeaways:

- Precision in an Increasingly Uncertain Market

The fourth quarter marks a critical juncture: the Federal Reserve cut rates as expected but signaled significant uncertainty about future easing, the government shutdown continues to disrupt transactions and erode confidence, and regional market variations have never been more pronounced. The market is transitioning, not recovering.

For appraisers, these conditions demand more than formulaic approaches. We must:

Prioritize recent comparable sales and explicitly discuss market trends between comparable sale dates and the effective date of value…

Our professional value lies in our ability to analyze complex market dynamics, exercise informed judgment, and provide well-supported opinions of value that reflect current market realities rather than outdated assumptions.

This is precisely the type of market environment where skilled appraisers demonstrate their value. Your expertise in navigating these nuances, from parsing Fed statements to quantifying shutdown impacts to identifying regional divergences, ensures credible valuations.

- Develop rigorous time adjustments using paired sales analysis and aggregate market statistics, recognizing that negative adjustments may be appropriate in some markets

- Analyze pending sales and active listings to capture current market direction that closed sales may not reflect

- Demonstrate command of local market conditions rather than relying on national narratives or Fed policy assumptions

- Carefully analyze buyer profiles in comparable sales to ensure they reflect the subject property’s most probable purchaser

To read more, Click Here

My comments: Written by an appraiser/economist for appraisers. I see a lot of articles on these topics, but this one I always read as it focuses on appraising.

I definitely think that national stats are not very useful for residential appraisals now, so I don’t often include them in these newsletters.

——————————————————————

HOW TO USE THE NUMBERS BELOW. Appraisals are ordered after the loan application. These numbers tell you the future for the next few weeks. For more information on how they are compiled, Click Here.

Note: I publish a graph of this data every month in my paid monthly newsletter, Appraisal Today. For more information or get a FREE sample go to www.appraisaltoday.com/order Or call 510-865-8041, MTW, 7 AM to noon, Pacific time.

My comments: We are all waiting for rates to drop lower in 2025/2026.

——————————————————–

Mortgage applications decreased 1.9 percent from one week earlier

WASHINGTON, D.C. (November 5, 2025) — Mortgage applications decreased 1.9 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending October 31, 2025.

The Market Composite Index, a measure of mortgage loan application volume, decreased 1.9 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 3 percent compared with the previous week. The Refinance Index decreased 3 percent from the previous week and was 151 percent higher than the same week one year ago. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 26 percent higher than the same week one year ago.

“Mortgage rate movements were mixed last week as Treasury yields moved slightly higher following last week’s FOMC meeting. The 30-year fixed rate was mostly unchanged at 6.31 percent and remained close to the lowest level in over a year,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “Despite a decline last week, refinance applications are still significantly higher than a year ago. The average loan size for refinance applications was at its highest level in six weeks, as borrowers with larger loans continued to seek ways to lower their monthly payments. Purchase applications declined slightly from a week ago, however, there was a slight increase in FHA purchase applications as prospective homebuyers continue to seek loan options to help manage challenging affordability conditions.”

The refinance share of mortgage activity decreased to 57.0 percent of total applications from 57.1 percent the previous week. The adjustable-rate mortgage (ARM) share of activity decreased to 8.7 percent of total applications.

The FHA share of total applications decreased to 18.5 percent from 20.5 percent the week prior. The VA share of total applications increased to 14.9 percent from 13.4 percent the week prior. The USDA share of total applications increased to 0.3 percent from 0.2 percent the week prior.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($806,500 or less) increased to 6.31 percent from 6.30 percent, with points remaining unchanged at 0.58 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans. The effective rate increased from last week.

The average contract interest rate for 30-year fixed-rate mortgages with jumbo loan balances (greater than $806,500) increased to 6.43 percent from 6.38 percent, with points decreasing to 0.33 from 0.34 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The average contract interest rate for 30-year fixed-rate mortgages backed by the FHA increased to 6.13 percent from 6.12 percent, with points remaining unchanged at 0.73 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The average contract interest rate for 15-year fixed-rate mortgages decreased to 5.65 percent from 5.67 percent, with points remaining unchanged at 0.61 (including the origination fee) for 80 percent LTV loans. The effective rate decreased from last week.

The average contract interest rate for 5/1 ARMs decreased to 5.56 percent from 5.66 percent, with points increasing to 0.86 from 0.51

The survey covers U.S. closed-end residential mortgage applications originated through retail and consumer direct channels. The survey has been conducted weekly since 1990. Respondents include mortgage bankers, commercial banks, thrifts, and credit unions. Base period and value for all indexes is March 16, 1990=100.

————————————————————————————–

Ann O’Rourke, MAI, SRA, MBA

Appraiser and Publisher Appraisal Today

1826 Clement Ave. Suite 203 Alameda, CA 94501

Phone: 510-865-8041

Email: ann@appraisaltoday.com

Online: www.appraisaltoday.com

We want to know what you think!! Please leave a comment.