Newz: Road to Housing Act and Appraisals, Florida Class Action: AMCs and Appraisal Fees

July 17, 2026

What’s in This Newsletter (In Order, Scroll Down)

- LIA AD: State Board Complaints: Does It Mean the End of Your Coverage?:

- Appraisal Provisions Included in the 21st Century ROAD to Housing Act

- Bargain $139K Shipping Container ‘Retreat’ in Virginia Proves You Should Never Judge a Book by Its Cover

- Appraiser Capacity, Updated June, 2026, Freddie Mac

- MY AD: Is Expert Witness a Viable Alternative to GSE Work By Tim Andersen, MAI

- Florida Class Action: What’s It Mean for Appraisers? by Isaac Peck, Publisher, Working RE

- Where Does an FHA Appraisal End and a Home Inspection Begin? HUD Has an Opportunity to Clarify. By Shane White, SRA

- MBA: Mortgage applications decreased 2.7 percent from one week earlier

———————————————–

Appraisal Provisions Included in the 21st Century ROAD to Housing Act

Appraisal Institute News Release, June 26, 2026

Editor’s Note: This is Now a Law.

Excerpts: The recently passed 21st Century ROAD to Housing Act (H.R. 6644), now awaiting Presidential signature, includes two appraisal-focused measures supported by the Appraisal Institute: the Appraisal Industry Improvement Act and the Appraisal Modernization Act. Together, these provisions represent the most significant federal appraisal legislation enacted in several years and address workforce development, regulatory oversight, consumer protections, and appraisal modernization.

Appraisal Industry Improvement Act

The Appraisal Industry Improvement Act contains several provisions designed to strengthen the appraisal profession, modernize oversight, and expand pathways into appraisal practice.

Topics include:

- Strengthening the Appraisal Subcommittee

- Entry into the Profession

- Expanded FHA Appraiser Eligibility and Training Requirements

- The legislation would allow both state-certified and state-licensed residential appraisers to perform FHA appraisals

- Appraisal Modernization Act primarily on consumer protections and appraisal transparency.

- Reconsideration of Value (ROV) Process

- Second Appraisal Procedures

- GAO Study of a Public Appraisal Database

And More

To read the full News release, Click Here

My comments: Many thanks to the Appraisal Institute for telling us what the new Housing Act means for appraisers. Definitely worth reading the full News release.

——————————————————————-

Bargain $139K Shipping Container ‘Retreat’ in Virginia Proves You Should Never Judge a Book by Its Cover

Excerpts: 3 bedrooms, 3.5 baths, built in 2024, That you see in a property listing is not always what you might get in the real-life home—and nowhere is that warning more prophetic than at a recently listed shipping container “retreat” in Virginia. This property tells two vastly different tales of what the future of the dwelling may hold.

The first images in the listing for the property, which is located in Stanardsville, VA, and is on the market for just $139,000, depict an idyllic mountain sanctuary with a modern façade, a stunning wood deck overlooking the surrounding woodland, and floor-to-ceiling windows that bathe the interiors of the home in natural light.

But upon closer inspection, those photos do not depict the state that the home is currently in. Rather, they show an AI-generated version of events that could unfold for a buyer who is willing to do some “heavy lifting” to turn that dream into a reality.

Scroll to the photos of the actual property, and the truth is starker than what AI would have you believe. The photos reveal little more than a bare shell composed of three containers that have not yet been set up to live in.

“Ready for a buyer with vision,” the eco-friendly retreat has stacked its way to the top of the week’s most popular homes list.

While the structures have been placed on a permanent foundation, they do not have heating, air conditioning, a kitchen, or even a bathroom in place. However, the listing makes clear that, for someone willing to roll up their sleeves and invest a fair amount of elbow grease into the ongoing construction of the home, it could, one day, be transformed into a truly spectacular residence.

To read the listing, Click Here

———————————————————–

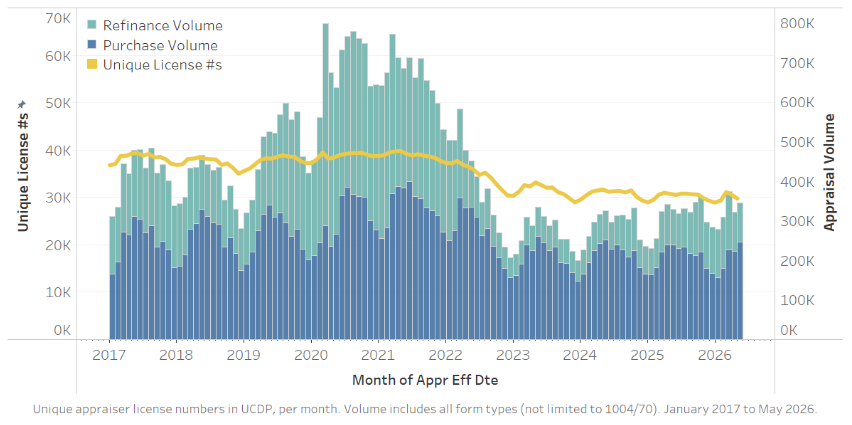

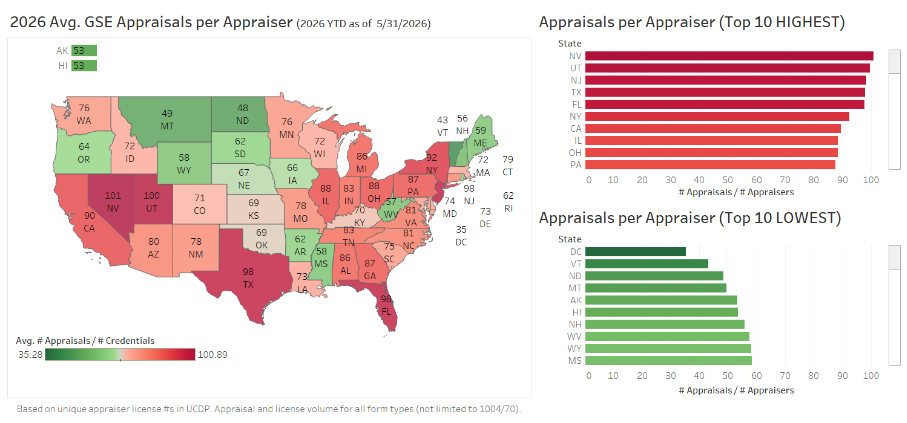

Freddie Mac Data Highlights Regional Differences in Appraisal Workload

Appraisal Institute, News release July 2, 2026

Excerpts: As the housing market continues to normalize following the unprecedented refinance boom of 2020 and 2021, a newly updated Freddie Mac analysis provides an interesting look at how appraisal activity is distributed across the country and what it may say about changing market dynamics.

The centerpiece of the report is a state-by-state heat map showing the average number of GSE appraisals completed per active appraiser credential during the first five months of 2026. Rather than measuring the number of appraisers in each state, the map illustrates average appraisal workload, revealing considerable variation from one market to another..

For the appraisal profession, the data underscore the importance of looking beyond national averages. Local housing conditions, demographic trends, and mortgage market activity all influence appraisal workloads, meaning that market conditions can differ significantly from one state, or even one metropolitan area, to another.

To see the original graphs (easier to read), Click here

To read the Appraisal Institute News Release, Click Here

My comments: What do you think about what the graphs say?

———————————————————-

Are you getting too many ad-only emails?

4 ways to get only the FREE email newsletters and NOT the ad-only emails.

1. Twitter: https://twitter.com/appraisaltoday Posted by noon Friday

2. Read on blog www.appraisaltoday.com/blog Posted by noon Friday. You can subscribe to the blog in the upper right of each blog page. NOTE: the popular ads with liability tips are below the first topic on my blog posts.

3. Email Archives: https://appraisaltoday.com/archives

(posted by noon Friday) The link is above and to the left of the big yellow email signup form. Newsletters start with “Newz.” Contains all recent emails sent.

4. Link to the 10 most recent newsletters (no ads) at www.appraisaltoday.com. Scroll down past the big yellow signup block. The newsletters have abbreviated titles, taken from their blog posts.

To read more about the 4 ways, plus information on why I take ads, etc.

—————————————————–

Is Expert Witness a Viable Alternative to GSE Work

By Tim Andersen, MAI

In the July issue of Appraisal Today

Excerpt: As GSE appraisal assignments continue declining in many American

markets, appraisers increasingly seek alternative revenue sources.

One increasingly attractive avenue involves expert witness work in

litigation support. That transition, however, demands substantial

retraining, expanded education, and disciplined methodological

development.

Courtroom appraisal work differs fundamentally from ordinary

mortgage lending assignments. The appraiser must prepare an

appraisal acceptable to judicial scrutiny. The appraiser must

communicate conclusions clearly and persuasively to attorneys,

judges, juries, and regulators. Most importantly, the appraiser must

survive aggressive professional cross-examination.

Litigation appraisal requires methodological transparency. The

expert witness must explain analytical reasoning clearly, logically, and

persuasively. Many appraisers struggle here because traditional

mortgage work rewards brevity more than analytical explanation.

Litigation work reverses that priority entirely.

To read the full article plus many more articles on non-lender appraisals, and 3+ years of previous issues, subscribe to the paid Appraisal Today at www.appraisaltoday.com/order .

Not sure if you want to subscribe?

Sign up for monthly auto renewal for $8.25!

Cancel at any time for any reason! You will receive a prorated refund.

$8.25 per month, $24.75 per quarter, and $89 per year (Best Buy)

or $99 per year or $169 for two years

Subscribers get FREE: past 18+ months of past newsletters

What’s the difference between the Appraisal Today free Weekly email newsletter and the paid Monthly newsletter? Click here for more info.

————————————————————

If you are a paid subscriber and did not receive the

July, 2026 issue emailed on

Wednesday, July 1, 2026 please email info@appraisaltoday.com, and we will send lt to you. You can also hit the reply button. Be sure to include a comment requesting it. Or, call 510-865-8041

———————————————————-

Florida Class Action: What’s It Mean for Appraisers?

by Isaac Peck, Publisher, Working RE

Excerpts: For the second time in just over a year, a class action lawsuit is challenging how appraisal management companies (AMCs) handle the fees borrowers pay for appraisals. Arnold v. Appraiser Nation, filed in a Florida federal court in December 2025, accuses Appraisal Nation, AMC Links, and United Wholesale Mortgage of charging borrowers appraisal fees that bear little relation to what the appraiser actually receives, and concealing the difference.

The case advances arguments similar to those in Timmins v. Clear Capital, Core Valuation Management, and Rocket Mortgage, the California class action lawsuit we covered in our Summer 2025 issue. But Arnold takes a different legal path. Where Timmins proceeds under California’s state consumer-protection statutes, Arnold frames its claims under the Real Estate Settlement Procedures Act of 1974, targeting RESPA’s prohibitions against unearned charges and fee-splitting in settlement services.

The timing is not coincidental. Many appraisers had looked to the Consumer Financial Protection Bureau (CFPB) to force separation of appraisal and AMC fees on consumer disclosures. That effort stalled when the agency’s authority was curtailed in early 2025. With federal rulemaking off the table, the pressure has shifted to the courts.

Calls for Reform from California to Florida

Both cases allege the same core facts: borrowers were overcharged, AMCs retained the majority of the fee, and the system was designed to prevent anyone from seeing the split. But their legal paths are different, and that difference matters. Timmins proceeds under California’s broad state consumer-protection statutes, which do not require proving a RESPA-style “unearned fee” or fee-splitting violation. Arnold must fit its theory into RESPA’s narrower framework while also overcoming the CFPB’s explicit acceptance of bundled appraisal/AMC fees and the fact that lenders, not AMCs, control TRID disclosures.

Regardless of how either case is ultimately decided, the direction is clear. AMCs and lenders are facing increasing pressure to justify bundled fee structures, and each new filing makes it harder for regulators to remain on the sidelines. For appraisers, greater transparency in how fees are disclosed to borrowers could ease the downward pressure that opaque AMC retention practices have created for more than a decade. Time will tell.

To read more, Click Here

My comments: This appraisal fee issue started when AMCs took over managing appraisals for lenders. Maybe it will finally be resolved!

————————————–

Where Does an FHA Appraisal End and a Home Inspection Begin?

HUD Has an Opportunity to Clarify.

By Shane White, SRA

Excerpts: he agency’s Request for Information on Minimum Property Requirements raises a question the industry has been slow to ask: not about which repairs to require, but about who the FHA appraiser is supposed to be.

On May 29, 2026, the Department of Housing and Urban Development published a Request for Information in the Federal Register asking stakeholders to weigh in on FHA’s Minimum Property Requirements, the standards that govern whether a single-family home qualifies for FHA-insured financing. Comments are due June 29, 2026 (Docket No. FR-6609-N-01).

The MPR framework has not undergone a comprehensive update since Mortgagee Letter 2005-48, over two decades ago. Many FHA appraisals still result in repair conditions or additional inspection requirements that create friction for first-time and lower-income buyers, precisely the population FHA exists to serve. Those are legitimate problems worth solving. But the most important question embedded in this RFI is not about which repair conditions to remove, or how closely FHA standards should align with Fannie Mae and Freddie Mac.

At what point does an appraisal stop being an appraisal?

That’s the question. And it deserves a more honest answer than the industry has offered so far.

Oddly enough, I don’t think this is really an MPR debate at all. It’s a role-definition debate that just happens to be playing out through the MPRs. A Profession That Has Changed Without Quite Saying So

For years, the appraisal profession has quietly absorbed additional responsibilities without much discussion about whether those responsibilities still fit within the traditional definition of an appraisal assignment.

The Line Has Moved

Most borrowers who go through an FHA transaction are told, at some point, that an appraisal is not a home inspection. Their real estate agent says it. Their loan officer says it. The appraiser may say it too. It appears in disclosures.

And then they find out what an FHA appraisal actually involves…

The Role Confusion Nobody Talks About

The ambiguity extends beyond property condition itself.

The Guidance Framework Has Not Kept Pace

Most working FHA appraisers can probably recall at least one call to the HUD Resource Center that produced more confusion than clarity.

Then There’s the Liability Side of This

What Appraisers Actually Bring to the Table

An FHA appraiser brings something to the transaction that no checklist can replicate. They evaluate the interaction between property condition and market behavior.

To read more, Click Here

My opinion: If you do FHA appraisals, read the full article. Very well written and understandable written by a practicing appraiser. I got on the FHA panel in 1986, when I started my business. I quit after a year or so – they wanted too much from appraisers. Maybe this will change. At least they were asking for comments.

HOW TO USE THE NUMBERS BELOW. Appraisals are ordered after the loan application. These numbers tell you the future for the next few weeks. For more information on how they are compiled, .

Note: I publish a graph of this data every month in my paid monthly newsletter, Appraisal Today. For more information or get a FREE sample go to www.appraisaltoday.com/order Or call 510-865-8041, MTW, 7 AM to noon, Pacific time.

My comments: Rates are going up and down. We are all waiting for rates to drop lower in 2027.

Mortgage applications decreased 2.7 percent from one week earlier

WASHINGTON, D.C. (July 15, 2026) — Mortgage applications decreased 2.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending July 10, 2026. Last week’s results included an adjustment for the Fourth of July holiday.

The Market Composite Index, a measure of mortgage loan application volume, decreased 2.7 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 8 percent compared with the previous week. The Refinance Index increased 4 percent from the previous week and was 7 percent higher than the same week one year ago. The seasonally adjusted Purchase Index decreased 7 percent from one week earlier. The unadjusted Purchase Index increased 3 percent compared with the previous week and was 2 percent lower than the same week one year ago.

“Mortgage applications declined as the 30-year fixed rate increased to 6.65 percent, the highest level since August 2025. Purchase applications were down over the week and dipped below last year’s pace in the week following the July 4th holiday,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “Despite higher mortgage rates, refinance applications increased, led by FHA and VA refinance applications rising 9 and 10 percent, respectively.”

The refinance share of mortgage activity increased to 43.2 percent of total applications from 40.6 percent the previous week. The adjustable-rate mortgage (ARM) share of activity decreased to 7.1 percent of total applications.

The FHA share of total applications increased to 17.7 percent from 16.4 percent the week prior. The VA share of total applications increased to 13.6 percent from 13.0 percent the week prior. The USDA share of total applications remained unchanged at 0.5 percent from the week prior.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($832,750 or less) increased to 6.65 percent from 6.58 percent, with points increasing to 0.67 from 0.64 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans. The effective rate increased from last week.

The average contract interest rate for 30-year fixed-rate mortgages with jumbo loan balances (greater than $832,750) increased to 6.62 percent from 6.50 percent, with points increasing to 0.54 from 0.42 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The average contract interest rate for 30-year fixed-rate mortgages backed by the FHA increased to 6.33 percent from 6.28 percent, with points increasing to 0.81 from 0.79 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The average contract interest rate for 15-year fixed-rate mortgages increased to 6.05 percent from 5.99 percent, with points increasing to 0.88 from 0.71 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The average contract interest rate for 5/1 ARMs decreased to 5.75 percent from 5.84 percent, with points decreasing to 0.93 from 0.94 (including the origination fee) for 80 percent LTV loans. The effective rate decreased from last week.

The survey covers U.S. closed-end residential mortgage applications originated through retail and consumer direct channels. The survey has been conducted weekly since 1990. Respondents include mortgage bankers, commercial banks, thrifts, and credit unions. Base period and value for all indexes is March 16, 1990=100.

———————————————————

Ann O’Rourke, MAI, SRA, MBA

Ann O’Rourke, MAI, SRA, MBA

Appraiser and Publisher Appraisal Today

1826 Clement Ave. Suite 203 Alameda, CA 94501

Phone: 510-865-8041

Email: ann@appraisaltoday.com

Online: www.appraisaltoday.com

We want to know what you think!! Please leave a comment.