Newz: Recent Executive Orders Affecting Appraisers, When Appraisers Take the Stand

June 12, 2026

What’s in This Newsletter (In Order, Scroll Down)

- LIA AD: A case of forgery

- Recent Executive Orders: Threat, Opportunity, or Both for Appraisers? By Kim Perotti, AXIS AMC

- $22.8 Million Aspen Home With Its Own Private Waterfall Feels Like a Real-Life Fairy Tale

- MY AD: If the Standards Are Uniform, Why Isn’t Your License? By Thaddus Dawson, Jr., CG

- When Appraisers Take the Stand By By David C. Wilkes, Esq., CRE, FRICS and Kevin M. Clyne, Esq., CRE

- Agents, Are You Using AI to Price Your Listings? By Tom Horn

- 10K Appraisers. Policy and Advocacy Day, By 10K Appraisers Foundation

- MBA: Mortgage applications increased 10.8 percent from one week earlier

Recent Executive Orders: Threat, Opportunity, or Both for Appraisers?

By Kim Perotti, a founding partner of AXIS AMC

Excerpts: In March 13, 2026, President Trump signed two Executive Orders that together amount to a clear message for our profession: build more houses, make credit easier, and get the valuation piece done faster and cheaper. We think it’s critically important that our industry discuss the implications.

The two orders are:

REMOVING REGULATORY BARRIERS TO AFFORDABLE HOME CONSTRUCTION

AND PROMOTING ACCESS TO MORTGAGE CREDIT

While they are not “about” appraisers, the Executive Orders will absolutely reshape the environment in which we work. Appraisers who treat these as background noise will find the ground shifting under their feet. Those who read them as a roadmap can pick their spots and come out stronger and, more importantly, help shape how they are put into practice.

REMOVING REGULATORY BARRIERS TO AFFORDABLE HOME CONSTRUCTION:

Faster, Cheaper Construction – What That Really Means for Your Desk

PROMOTING ACCESS TO MORTGAGE CREDIT: Faster, Cheaper Valuations – Where the Squeeze Shows Up – Second Order

The second order takes direct aim at how loans—and valuations—get done. The theme is unmistakable: streamline, digitize, and de-emphasize technical compliance.

For appraisers, here are the potential realities:

More alternative valuation products: Regulators are being encouraged to expand the use of AVMs, desktop, and hybrid appraisals and reduce full appraisal requirements on low-risk and small-balance loans. You should expect more hybrid and desktop requests and data-only products as well as a clearer dividing line between high-volume, low-margin work and complex, higher-risk assignments.

Pressure on fees and turn times: Agencies are being asked to set “clear appraisal timelines” and cut costs and therefore lenders will likely lean harder on speed and price whenever a waiver, AVM, or hybrid is allowed, and traditional assignment ordering will have to justify itself on risk grounds.

Changes in who can appraise and how: The order invites simplification of appraiser qualification requirements. Easier entry could mean more competitors and lenders may fill low-fee niches with less-experienced personnel or non-traditional vendors.

If your business is built primarily on simple, low-risk assignments, this is a direct competitive challenge.

Alignment of FHA and VA rules: HUD and VA are asked to align standards where risk is comparable, clarify what truly requires pre-closing repairs vs. what’s cosmetic, and expand post-closing repair flexibility.

That could change the frequency and scope of “subject to” conditions, reduce some friction and disputes around FHA/VA appraisals, and make your judgment about safety vs. cosmetic issues more visible and important.

In summation, this order calls for more technology and alternatives, more pressure on traditional appraisals, and more segmentation of valuation products by risk level.

A Clear Fork in the Road for Appraisers

Taken together, these two Executive Orders point in one direction: more volume, more complexity at the edges of the market, and more pressure to commoditize anything that looks “low risk.” Together they create a fork in the road for real estate appraisers:

If you stay in the lane of interchangeable, low-complexity assignments, you will feel the squeeze—from technology, from relaxed standards, and from new entrants.

If you lean into complexity—new construction, manufactured and modular, fringe markets, environmental and hazard issues, FHA/VA nuance—you become harder to replace, not easier.

This doesn’t mean abandoning efficiency or refusing alternative products. It means being fluent in hybrids and desktops so you can decide which work makes sense for you, positioning yourself as the expert when a lender can’t responsibly rely on an AVM or a waiver, and building documented expertise in the exact areas these orders will expand.

To read more, Click Here

My comments: Definitely worth reading. All about what this means for appraisers in detail. The best analysis for appraisers I have read about this executive order. The author is definitely an “insider” as she is Co President of AXIS, a long time AMC. When I wrote one of my first articles on AMCs, I interviewed AXIS.

——————————————————–

$22.8 Million Aspen Home With Its Own Private Waterfall Feels Like a Real-Life Fairy Tale

Excerpts: 5 bedrooms, 5.5 baths, 5,294 sq.ft., 0.86 acre lot, built in 1974

Mountain views and luxury interiors are practically a given in the upscale Colorado resort of Aspen, but a private waterfall cascading under your living room? That’s quite rare, to say the least.

Yet that is exactly what’s on offer at the aptly named 87 Magnifico Drive, an extraordinary property that is perched atop Aspen’s Lower Red Mountain but looks like it was dropped straight out of the pages of a fairy tale.

The idyllic home has recently returned to the market with a price tag of $22.75 million, a significant reduction after its initial debut at $29.95 million. And while Aspen is no stranger to trophy properties, this one, which is listed with Mandy Welgos of Sotheby’s International Realty, is particularly special.

Indoor-outdoor living is at its best with expansive patios and beautifully landscaped gardens framed by tranquil waterfalls.

To read the listing with 46 photos, aerial views and 3D views, Click Here

—————————————————————–

When Appraisers Take the Stand

By David C. Wilkes, Esq., CRE, FRICS and Kevin M. Clyne, Esq., CRE

Excerpts: Real estate appraisers have long played an essential role in litigation involving property valuation. Courts frequently rely on experienced valuation professionals to provide independent opinions in disputes ranging from eminent domain and property tax appeals to partnership disputes, lender litigation, insurance claims, and complex commercial real estate matters. In many of these cases, the court depends on the appraiser to translate market evidence into a clear and reliable opinion of value.

In today’s environment, the legal landscape surrounding expert testimony has become more demanding. Courts are applying greater scrutiny to expert methodologies, litigants are increasingly aggressive in challenging valuation opinions, and expert witnesses face growing exposure to regulatory complaints and civil liability. For appraisers who accept litigation assignments, understanding these evolving risks is now an important part of professional practice—particularly for those working in insurance, financial, and risk-management related matters where valuation conclusions can have significant financial consequences.

Courts now routinely evaluate the reliability of expert testimony before allowing it to be presented at trial. Judges often examine whether an expert’s methodology is grounded in accepted appraisal principles and whether those principles were applied appropriately to the facts of the case.

For valuation professionals, this scrutiny frequently focuses on several core components of the appraisal process:

• Selection of comparable transactions

• Support for adjustments

• Highest and best use analysis

• Treatment of market conditions

• Reconciliation of valuation approaches

To read more, Click Here

My comments: Excellent detailed discussion of issues in expert witness testimony. I have done expert witness testimony. This is worth reading, just in case the opposing attorney knows what is in this article! I have been lucky and did not ever have an opposing attorney who knew much about appraisals.

——————————————————————-

Are you getting too many ad-only emails?

4 ways to get only the FREE email newsletters and NOT the ad-only emails.

1. Twitter: https://twitter.com/appraisaltoday Posted by noon Friday

2. Read on blog www.appraisaltoday.com/blog Posted by noon Friday. You can subscribe to the blog in the upper right of each blog page. NOTE: the popular ads with liability tips are below the first topic on my blog posts.

3. Email Archives: https://appraisaltoday.com/archives

(posted by noon Friday) The link is above and to the left of the big yellow email signup form. Newsletters start with “Newz.” Contains all recent emails sent.

4. Link to the 10 most recent newsletters (no ads) at www.appraisaltoday.com. Scroll down past the big yellow signup block. The newsletters have abbreviated titles, taken from their blog posts.

To read more about the 4 ways, plus information on why I take ads, etc.

If the Standards Are Uniform, Why Isn’t Your License?

In the June, 2026 issue of Appraisal Today

By Thaddaus Dawson, CG

Excerpts: Let me ask you something that every appraiser reading this has lived but perhaps never named out loud.

If the standards governing your work are truly uniform, if every appraiser in

America is tested on the same national examination, trained on the same USPAP framework, and evaluated against the same qualification criteria, then why does your license not transfer across state lines without a fee, a waiting period, and a bureaucratic prayer?

The answer to that question is the answer to everything wrong with this profession for the past 38 years.

The Appraiser Qualifications Board presented the results of a national job study of 3,691 appraisers surveyed across all 50 states and the District of Columbia. The findings were definitive. Appraisers in every state perform the same job, at the same frequency, rated at the same level of importance. The data is not ambiguous.

The job is uniform. The examination is uniform. The standards are uniform.

But the enforcement is not. And that is the delusion that has governed this

profession since 1989.

To read the full article, plus 3+ years of previous issues, subscribe to the paid Appraisal Today at www.appraisaltoday.com/ .

Not sure if you want to subscribe?

Sign up for monthly auto renewal for $8.25!

Cancel at any time for any reason! You will receive a prorated refund.

$8.25 per month, $24.75 per quarter, and $89 per year (Best Buy)

or $99 per year or $169 for two years

Subscribers get FREE: past 18+ months of past newsletters

What’s the difference between the Appraisal Today free Weekly email newsletter and the paid Monthly newsletter? Click here for more info.

———————————————-

If you are a paid subscriber and did not receive the

June, 2026 issue emailed on

Monday, June 1, 2026 please email info@appraisaltoday.com, and we will send it to you. You can also hit the reply button. Be sure to include a comment requesting it. Or, call 510-865-8041

——————————————————–

Agents, Are You Using AI to Price Your Listings?

By Tom Horn

Excerpts: Don’t Let AI Kill Your Next Deal

You knew it was going to happen. Everybody is using AI to answer questions, help them write better, and create ultra-realistic photos and videos. It was just a matter of time before someone asked AI what their home is worth or how much a home should be listed for.

To accurately price, or appraise, a property, local knowledge and expertise are needed. This knowledge is needed to choose the right data and to apply judgment to the information. To be blunt, AI does not have this type of ability. Not yet, anyway. It’s also important for the user of the AI model to know the right questions to ask.

Getting back to my recent experience, it turns out that the information the AI model collected to support its value suggestion was inaccurate. In addition, some of the “comps” were not even in the subject property’s competitive market area. All of this combined resulted in the property being priced too high. The appraisal came in lower than the contract, and while the property did sell, it was for much lower than the list and contract price.

Speaking of square footage, one of the issues I saw with the square footage that AI used in my example was that it combined all of the living areas together. It added the heated and cooled areas in the basement to the above-grade area, which is a big no-no.

While all areas of a house are included in the final value, the basement area typically contributes a different amount than the main levels. If you combine them and apply a single price per square foot adjustment, the basement may be overvalued.

These inaccuracies will be found out if an appraisal is required for financing by the buyer. The appraiser will separate the basement area from the above-grade area, which can result in differences between the appraisal and contract price.

The data AI relies on can be wrong

Just like the infamous Zillow Zestimate, AI uses information from public records, like square footage. Public records are famous for having incorrect square footage information on a house.

If you rely on public records for the property you are pricing and the comps, that is a double whammy. The price per square foot of a sale that is calculated by dividing the sale price by the square footage can be wrong, and then if you multiply that by the incorrect square footage of the subject property, that can result in a property value indication that has no resemblance to reality.

To read more, Click Here

My comments: Definitely worth reading to understand how home owners and real estate agents may be using AI, typically a chatbot. Then you can explain why AI does not work well.

————————————————————

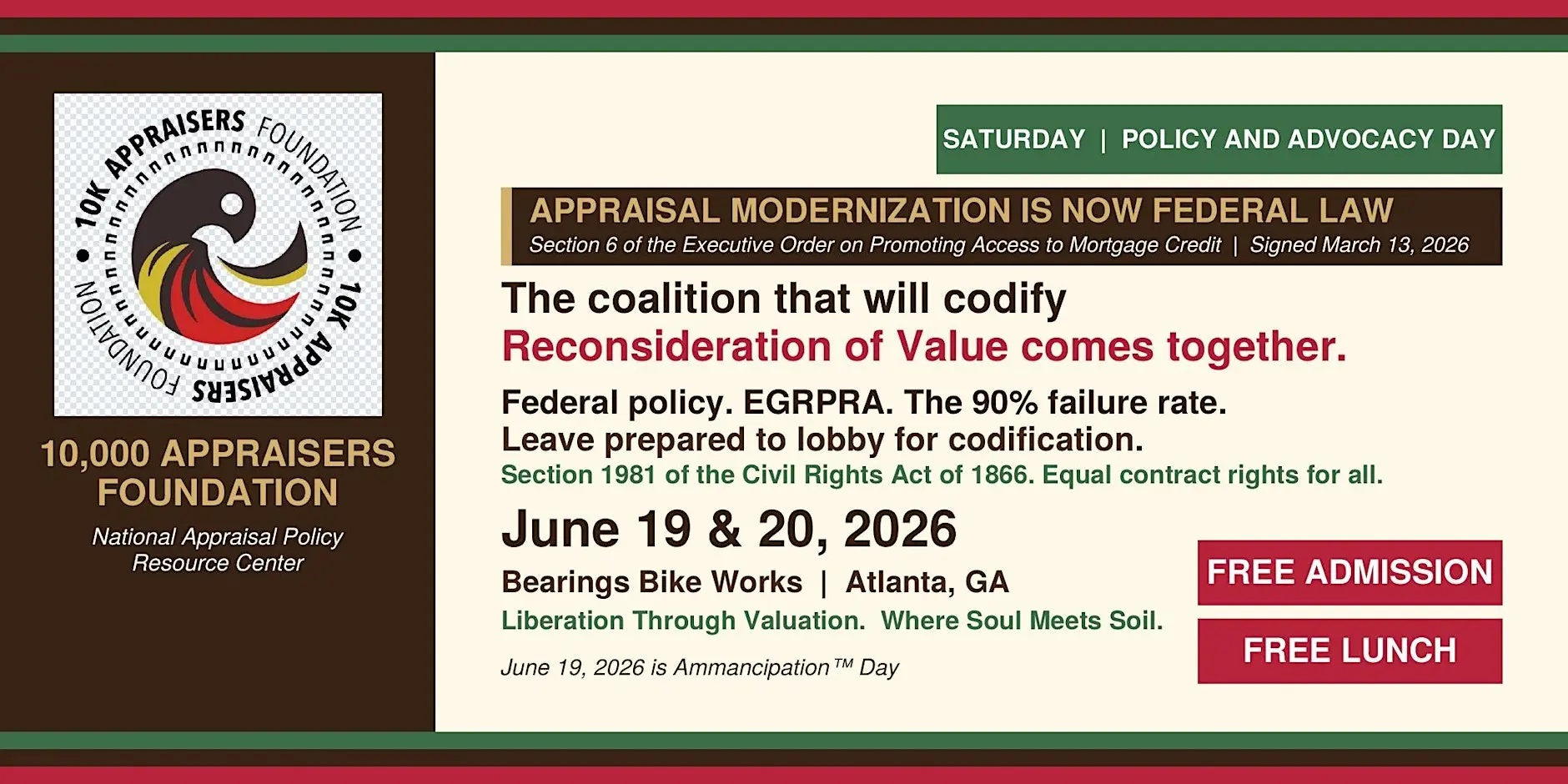

Policy and Advocacy Day, By 10K Appraisers Foundation

Saturday, June 20• 9 AM – 4 PM

The coalition that will codify Reconsideration of Value comes together.

Overview

You will learn about the federal policy impacts of the Executive Order Section 6 Appraisal Modernization, to correct the 90% FHFA failure .

Saturday, June 20, 2026 is the Policy and Advocacy Day.

Saturday is where the coalition that will codify Reconsideration of Value comes together. You will learn about the federal policy impacts of the President’s Executive Order on Section 6 Appraisal Modernization, the EGRPRA testimony record, the May 11 coalition letter, the 90 percent FHFA failure rate, and the structural reforms the 10,000 Appraisers Foundation has placed in the permanent congressional record. You leave Saturday prepared to lobby your members of Congress and your state legislators for the codification of Reconsideration of Value under Section 1981 as a universal contract protection for all Americans.

The mission.

This is the coalition that will build the Federal Appraisal Enforcement Authority, secure the Single National Appraisal License, and finally extend the protection roughly 17 million American veterans already enjoy to the more than 260 million American adults currently without it.

Come witness the profession that shows up.

Ammancipation Day. Atlanta. June 19 and 20, 2026.

Liberation Through Valuation: Where Soul Meets Soil.

Saturday is for the appraisers

To read more about the event and register, Click Here

For more info on the founder and organizer, Thaddaus Dawson, CG, Click Here

My comments: I published his excellent article “Miseducation of the Appraiser Series”, in the June 2026 issue of Appraisal Today. Read an excerpt from the article he wrote above. He is well known as an advocate for challenging and changing ROVs.

———————————————————

HOW TO USE THE NUMBERS BELOW. Appraisals are ordered after the loan application. These numbers tell you the future for the next few weeks. For more information on how they are compiled, Click Here.

Note: I publish a graph of this data every month in my paid monthly newsletter, Appraisal Today. For more information or get a FREE sample go to www.appraisaltoday.com/order Or call 510-865-8041, MTW, 7 AM to noon, Pacific time.

My comments: Rates are going up and down. We are all waiting for rates to drop lower in 2027.

Mortgage applications increased 10.8 percent from one week earlier

WASHINGTON, D.C. (June 10, 2026) — Mortgage applications increased 10.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending June 5, 2026. Last week’s results included an adjustment for the Memorial Day holiday.

The Market Composite Index, a measure of mortgage loan application volume, increased 10.8 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 21 percent compared with the previous week. The Refinance Index increased 15 percent from the previous week and was 20 percent higher than the same week one year ago. The seasonally adjusted Purchase Index increased 7 percent from one week earlier. The unadjusted Purchase Index increased 17 percent compared with the previous week and was 4 percent higher than the same week one year ago.

“Mortgage rates were volatile last week as news from the Middle East continues to drive markets,” said Mike Fratantoni, MBA’s SVP and Chief Economist. “While the average rate was up slightly, with the 30-year fixed rate now at 6.60 percent, there were opportunities where borrowers were seeing somewhat lower rates. Both refinance and purchase applications rebounded coming out of the Memorial Day holiday week, with refinance applications up 15 percent and purchase applications up 7 percent.”

The refinance share of mortgage activity increased to 40.2 percent of total applications from 38.0 percent the previous week. The adjustable-rate mortgage (ARM) share of activity increased to 8.6 percent of total applications.

The FHA share of total applications increased to 17.4 percent from 17.0 percent the week prior. The VA share of total applications decreased to 13.4 percent from 14.4 percent the week prior. The USDA share of total applications decreased to 0.4 percent from 0.5 percent the week prior.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($832,750 or less) increased to 6.60 percent from 6.57 percent, with points decreased to 0.63 from 0.67 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans. The effective rate increased from last week.

The average contract interest rate for 30-year fixed-rate mortgages with jumbo loan balances (greater than $832,750) remained unchanged at 6.66 percent, with points increasing to 0.54 from 0.35 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The average contract interest rate for 30-year fixed-rate mortgages backed by the FHA increased to 6.27 percent from 6.26 percent, with points increasing to 0.78 from 0.75 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The average contract interest rate for 15-year fixed-rate mortgages increased to 5.99 percent from 5.93 percent, with points decreasing to 0.68 from 0.76 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The average contract interest rate for 5/1 ARMs increased to 5.96 percent from 5.82 percent, with points decreasing to 0.75 from 0.88 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The survey covers U.S. closed-end residential mortgage applications originated through retail and consumer direct channels. The survey has been conducted weekly since 1990. Respondents include mortgage bankers, commercial banks, thrifts, and credit unions. Base period and value for all indexes is March 16, 1990=100.

——————————–

Ann O’Rourke, MAI, SRA, MBA

Ann O’Rourke, MAI, SRA, MBA

Appraiser and Publisher Appraisal Today

1826 Clement Ave. Suite 203 Alameda, CA 94501

Phone: 510-865-8041

Email: ann@appraisaltoday.com

Online: www.appraisaltoday.com

We want to know what you think!! Please leave a comment.