There is a lot of misinformation about CU. No one knows what will happen when CU is fully implemented. I speculate myself. I am an appraiser. I have opinions ;>

UAD is mechanical. CU is asking appraisers to think about their appraisals, not how to classify a characteristic.

For the appraisal profession, I think CU will make us better appraisers by making us take a critical look at adjustments. It will also help get rid of the “bad apples”, including appraisers that “push” values, throw anything into the form to get it out the door, need lots more training and education, etc.

I think Fannie’s main purpose of CU may be to stop appraisers from having low (or high) adjustments, inappropriate comps, using Q/C ratings, etc. to make values higher. That is what they worry about.

Only using comps from within the subject’s census tract is ridiculous and I’m sure CU will not be doing this. It is a good idea to see which census tracts match the neighborhood boundaries that you use. Or, part of Census Tracts. Then you can put the census tracts you use in your appraisal. In some areas census tracts are way out of date due to new construction, plus other problems.

To find census tracts near any property, go to http://www.huduser.org/qct/qctmap.html and type in an address.

I started my business in 1986 and had to put census tract numbers in my appraisals for the first time. I had previously worked for an assessor’s office and had never done a lender appraisal. I used Thomas Brothers Census Tract books to find them. To me, they often represented a reasonable way to delineate all, or part of, a neighborhood. Looking at the current census map for Alameda, CA, my city (population 75,000), it definitely did a good job of defining neighborhoods. However, I usually have to include more than one census tract as there is not enough data to do an appraisal otherwise. It did miss one very important neighborhood where most of Alameda’s large historic homes are located. There is a significant premium for being in this neighborhood. I very, very seldom go out of this neighborhood for comps. I suspect there are issues like this in other geographic areas. I have no idea what area Fannie would use, so I would put an explanation in my appraisal.

The problem is the forms, which were developed for use on tract homes. If you are not appraising a conforming tract home, it is like trying to put square boxes into round holes.

Every appraisal will have a risk score. A high risk score (1.0 to 5.0, where 5.0 is high risk) does not mean an appraisal is “bad”. It may be in an area of declining values or have a negative location problem. Or, not enough comps to provide a reliable value.

Remember that only certain UAD items will be considered by CU for now. If it is not UAD formatted, it will not be looked at. I don’t think Fannie’ use of census tracts will be the issue.

The Big Issue is support for adjustments. I have no idea how to support all the adjustments I make in my appraisals. I know what buyers will pay more, or less, for. But, I don’t know the exact dollar amount.

Regression is just one way to support adjustments, but it will not work for many adjustments, particularly if there are very few sales. Regression is not the only answer. There are many other methods. I will be writing about them in my paid email newsletters.

Regression works very well for time adjustments. Be sure yours are market based, not just from an MC form.

I am seriously considering not making any dollar adjustments when I use form reports for non-lending work, except time adjustments. I never make dollar adjustments on narratives and apartment form reports. My state regulator wants to see support in my files for adjustments.

Just because there is a box does not mean it has to be filled in. Qualitative adjustments are fine. There was a Fannie form developed and used for awhile in the 80s or early 90s that did not use dollar adjustments, only plus or minus signs. I worry about that a lot. The old Fannie 2-4 unit form did not have any adjustment boxes. I really hated when they changed that form to include adjustment boxes and de-emphasize the Income Approach.

No one knows how CU will work out. Will everyone turn down appraisals except for conforming tract homes? Will there be no one to do the tough appraisals and work in rural areas. When appraisers are compared, does the majority opinion win?

Will the days of 24 hour turn times and $200 fees be gone? Will AMCs stop broadcasting all appraisal orders to everyone on their fee panels? Will all appraisers be seen as the same and interchangeable? Or, will appraisers be rated on skills, education and experience? Will fees go up? Will fees be based on difficulty of the appraisal? Will lots of appraisers abandon the lender appraisal ship of fools?

Read the webinar pdfs and look at the maps from the two Fannie Webinars to see what they actually are doing. I spent lots of hours doing this, plus speaking with others about what they thought. Of course, it was for a 12-page article in my paid newsletter. Plus 18 pages of excerpts from Fannie documents and webinars. I probably would not have done it otherwise ;>

Go to www.fanniemae.com/singlefamily/collateral-underwriter and listen to Fannie’s two webinars for underwriters – very good with excellent illustrations and explanations. Plus, read the FAQs. You need to register, but it is very easy and you go directly to the webinar and can return at any time. There are lots of links on the web page for more information.

Last month’s January 2015 issue of the paid Appraisal Today newsletter had a 12-page article on CU plus 18 pages of addenda material. The February and subsequent issues will address problems such as how to make adjustments. Click the ad below for more information.

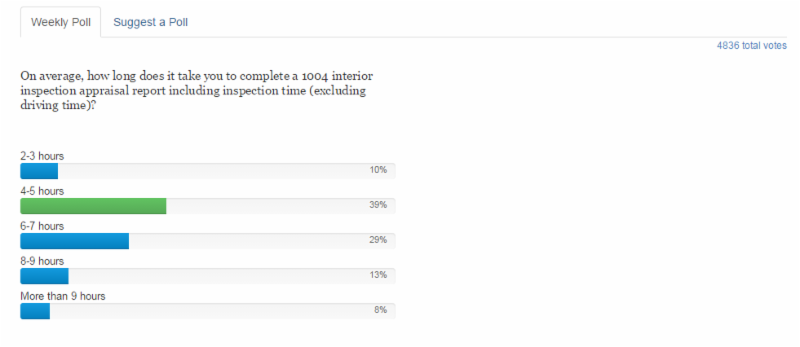

My comment: I have been hearing about scope creep causing increased appraisal report writeup times but now there is some data. Significantly increased, and still increasing from pre-AMC days. My non-lender report writing time has not changed since before HVCC. Appraisalport is a lender portal, so I guess there are some appraisers that write fast and others that write slow. Or, maybe it depends on your clients. AMCs tend to combine the requirements of multiple lenders into very long lists of requirements.

My comment: I have been hearing about scope creep causing increased appraisal report writeup times but now there is some data. Significantly increased, and still increasing from pre-AMC days. My non-lender report writing time has not changed since before HVCC. Appraisalport is a lender portal, so I guess there are some appraisers that write fast and others that write slow. Or, maybe it depends on your clients. AMCs tend to combine the requirements of multiple lenders into very long lists of requirements.