To keep up on what is happening in appraisal businesses, mortgage lending, USPAP, etc. , Plus humor and strange homes, sign up for my FREE weekly appraisal email newsletter, sent since June 1994. Go to Home on the left side of the menu at the top of this page or go to www.appraisaltoday.com

Sign up in the Big Yellow Boxes

I regularly write about hot topics in appraising and appraisal business management issues

in my paid Appraisal Today monthly newsletter.

$99 per year or (credit card only) $8.25 per month, $24.75 per quarter, or $89 per year.

For more info, go to https://www.appraisaltoday.com/products

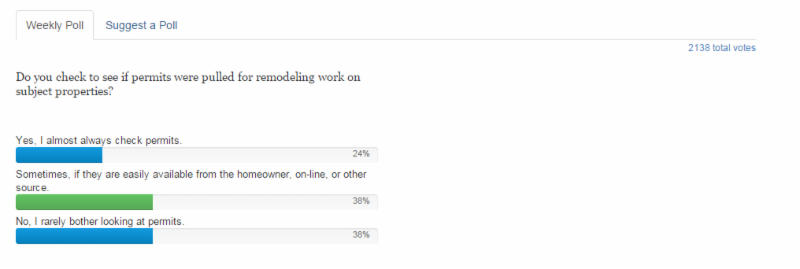

POLL: Do you check to see if permits were pulled on remodeling on subject properties? January, 2016

Source: www.appraisalport.com

My comment: A controversial topic. I’m not surprised at the results. However, if permits are online and free I don’t know why appraisers would not get them. In my city, free online records only go back to about 1970. Most of the homes were built before 1940. It costs $15.25 to get a full permit history and it can take up to a week to get it. The old records are a bit flakey, such as “remodeling” or something else very obscure. Lots and lots of unpermitted work in my city. But, in nearby cities with a lot of tract homes built since 1950, work without permits is not done very often. I was told by a lender’s chief appraiser many years ago not to pull permits so the borrower would “not get into trouble”.For quite awhile, I have been pulling the old permits when needed and run the online permits on all properties. In other cities, if something does not “look right”, such as an addition, I pull the permits.