FHA says no significant changes from previous requirements

My comment: I have heard from knowledgeable appraisers and instructors that there are few changes from the old handbook.

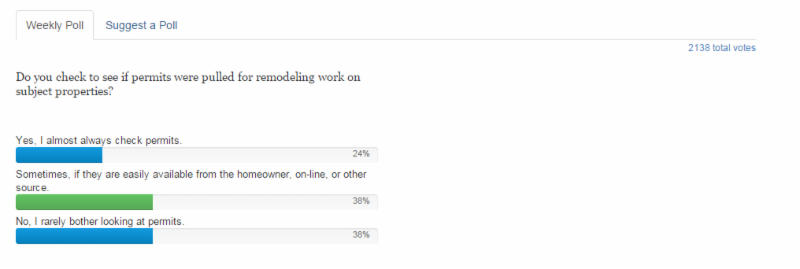

Recent posting by Coleen Morrison on a Facebook group

I heard back from my contact at HUD, and here is what she said: “Ms. Conde [the author of the article] (Ed note: see below) and I have had multiple conversations. FHA has not changed any of its requirements regarding the items that she discusses. If an FHA appraiser was compliant prior to September 14, the appraiser is going to be compliant after. The language has changed a bit, mostly for clarity and format, but the requirements are the same.”

I have written back and asked specifically about their thoughts regarding the Competency Rule. I have been saying the same thing … that nothing has really changed… but I never thought about the Competency Rule. It seems very contradictory when the HUD manual states the appraisal is not to be considered a home inspection;

…

The handbook states: “FHA appraisals are not a guarantee that the property is free from defects. The appraisal establishes the value of the property for mortgage insurance purposes only. Buyers need to secure their own home inspections through the services of a qualified inspector and satisfy themselves about the condition of the property.”

Adding the statement from the manual into your appraisals, and referencing Assumption and Limiting Condition #5 are 2 steps you can take to help protect yourself. I don’t know how much of a fight we can have against HUD, so if you choose to do FHA appraisals, and you were not doing the extent of inspection which is very clear in the 4001 now, you will need to step it up; add what the HUD manual states above in big bold letters to your report; or choose not to do FHA appraisals. The ultimate choice is yours.

My comment: I quit doing FHA appraisals in 1988, after 2 years on the roster. Too many requirements as compared with conventional. Plus… our local property values had skyrocketed way above the FHA limits… not much work.

————————————–

FHA vs USPAP – Appraisers Caught in Catch 22

By Joanne Conde

Excerpts:

The new FHA Handbook will become effective on September 14, 2015. There has been much discussion of the implications of changing “should” to “must” in thousands of examples in the Handbook. As a Board member of the Arizona Association of Real Estate Appraisers as well as being on the FHA Roster, I have taken a good hard look at these requirements and then, it hit me as I was teaching the Uniform Standards of Professional Appraisal Practice (USPAP) which is the basis of appraisal standards for every appraiser in the United States. The FHA assignment conditions, whether under “should” to “must” force appraisers into a Catch 22 or turn down the FHA appraisal assignments. FHA is essentially making it a condition of employment that appraisers violate the Competency Rule. Why did I not see this before? I guess because the two never converged in my mind at the same time and I expect that is what has also happened to other appraisers.

It is an FHA assignment condition that appraisers make the following statement within the report: “The utilities were on and functioning at the time of inspection and the home meets 4150.2 & 4905.1 HUD Requirements,” and “Other intended users[of the report] are HUD/FHA.”

Click here to read more and read appraisers’ comments