To keep up on what is happening in appraisal businesses, mortgage lending, USPAP, etc. , Plus humor and strange homes, sign up for my FREE weekly appraisal email newsletter, sent since June 1994. Go to Home on the left side of the menu at the top of this page or go to www.appraisaltoday.com

Sign up in the Big Yellow Boxes

I regularly write about hot topics in appraising and appraisal business management issues

in my paid Appraisal Today monthly newsletter.

$99 per year or (credit card only) $8.25 per month, $24.75 per quarter, or $89 per year.

For more info, go to https://www.appraisaltoday.com/products

Appraisalport polls on comp photos from June 2015

By Steve Costello,

This month I want to discuss three recent polls dealing with comp photos. In the first poll, we asked “With the availability of MLS photos, do you still feel it is necessary to drive by and photograph every comp?” We had a total of 3819 responses and the top two answers were very close. The winner, with 40 percent of the vote, was “Sometimes, it depends on the complexity of the specific assignment.” Coming in a close second was “Yes, I always want to see any property I use in a report” with 38 percent of the vote. The final answer of “No, I would rather just use MLS photos” only scored about half the votes as the first two answers, finishing with 22 percent. This makes sense because I think most appraisers want to look at a comp before they include it in a report, especially if they aren’t already familiar with the property. I can also see where some appraisers are very familiar with the properties in their area, use many of the same comps over and over again, and don’t feel a need to drive by and photograph them every time they use them.

In the next poll, we asked “In your opinion, with MLS, Google, and other photo sources available to clients, the main reason original comp photos are required from the appraiser is:” This poll had 3986 responses and had a pretty clear winner. A full 63 percent of the appraisers chose the answer “To make sure the appraiser actually drives by the comps.” So it looks like most appraisers don’t think their clients care as much about the actual photo compared to just making sure the appraiser actually visited the comp. The answer we expected to be very popular, “To provide the client with up-to-date photos of the comps – ensuring they exist in the stated condition,” only received 22 percent of the vote. A third response of “So the clients won’t have to take the time to look up the photos from one of the sources noted above” didn’t do well, only pulling in 3 percent of the vote. Not a surprise — we didn’t really expect many appraisers to choose that answer. Finally, 13 percent of appraisers went with “Other reason” as the best choice for this question. We really don’t know if there were one or many “other reasons” or what they are.

Finally, we asked “Would you be in favor of eliminating the requirement to include an original photo of every comp as long as a recent MLS photo of the property could be included with your report?” This question was very popular with 4770 total votes. It also produced a landslide vote with 79 percent of the appraisers selecting the answer “Yes.” Only 15 percent answered “No” and would not want to use an MLS photo instead of an original if it were available. A final 6 percent were “Not sure” how they felt about this issue. So, from this poll it is clear that appraisers feel that an original photo is not a necessity to produce a quality appraisal as long as a good representative photo is available from another source like an MLS.

My comment: As we all know, a photo taken at the time of listing from the MLS is often better than one taken later and USPAP does not require comp photos. Fannie Mae certifications require that the appraiser inspect the exterior of the comp, not take a photo. What about re-using a comp photo? Why the requirement of an “original” photo? To be sure appraisers drive by the comps.

Appraisal Humor

Appraisal business tips

A very, very funny appraiser video!

What does it cost to take appraisal comp photos?(Opens in a new browser tab)

Poll – Taking comp photos?(Opens in a new browser tab)

Posted in:

appraisal,

comp photos,

Fannie,

lender appraisals

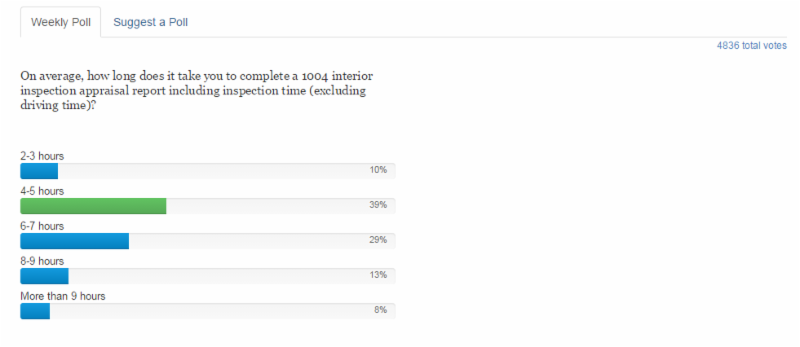

My comment: I have been hearing about scope creep causing increased appraisal report writeup times but now there is some data. Significantly increased, and still increasing from pre-AMC days. My non-lender report writing time has not changed since before HVCC. Appraisalport is a lender portal, so I guess there are some appraisers that write fast and others that write slow. Or, maybe it depends on your clients. AMCs tend to combine the requirements of multiple lenders into very long lists of requirements.

My comment: I have been hearing about scope creep causing increased appraisal report writeup times but now there is some data. Significantly increased, and still increasing from pre-AMC days. My non-lender report writing time has not changed since before HVCC. Appraisalport is a lender portal, so I guess there are some appraisers that write fast and others that write slow. Or, maybe it depends on your clients. AMCs tend to combine the requirements of multiple lenders into very long lists of requirements.