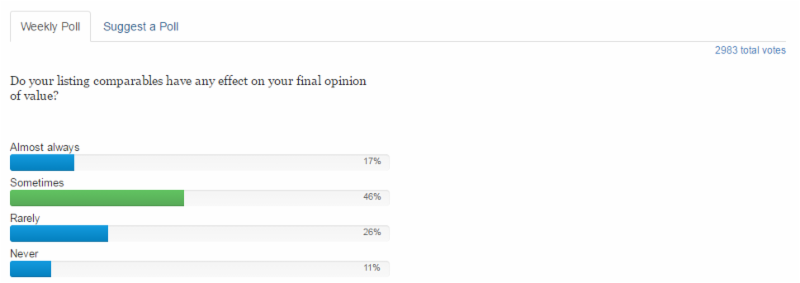

A Few CU Factoids

– Not all loans go to Fannie – VA, FHA, jumbo, etc.

– Fannie guidelines, including CU, are the minimum. Lenders can add their own, even keeping 15-25% adjustments.

– Lenders are not required to use CU.

– CU sends out appraisal warning messages for adjustments on: GLA, lot size, view, condition, quality, and location. For now.

– Gradual implementation of CU’s web based interface, which has the infamous “20 comps”, mapping, etc. Not available to AMCs.

A few CU comments and opinions from me:

– I need a Book of Adjustments!!! Maybe a few of Fannie’s will “leak” – wiki leaks ;>

– AMCs are now asking for adjustment support from non-CU adjustments. More Scope Creep??

– Mass confusion on what gets sent from underwriter to AMC to appraiser – warnings, Risk Scores, etc.

– The recent Fannie Letter to Lenders about CU said that the intent is not to overwhelm appraisers with warning messages. But, are underwriters going to read (and understand) 30+ page appraisals? I’m glad I’m not an underwriter!!

– How to respond to warning messages – not clear.

– Requests from AMCs include CU and non-CU requests. Sometimes hard to tell where they are from.

Adjustments – the “Dirty Little Secret” of Fannie Form Appraisal Reports

I can’t think of any time a client asked me for my support on an adjustment prior to CU. They have been accepting the usual responses, which are in many boilerplates: Based on my many years… or matched paired sales… etc.

A critical issue to me is that the dollar adjustments seem to indicate that residential appraisal values are precise and very accurate, which is not correct. There are lots of factors affecting home sales as compared with income property such as apartments and commercial property.

I have asked many very experienced appraisers how they “support” adjustments. Most use “rules of thumb”, such as using a percent of price per sq.ft. for GLA. But, this number includes land. Or, they use adjustments they were given when they were new appraisers. Of course, if you only appraise conforming homes in conforming tracts built in the past 10 years, it is much, much easier.

For now, CU only sends out warning messages for these adjustments: GLA, lot size, view, condition, quality, and location. This is a very small percent of all the UAD coded data. Plus, some data is not UAD coded, such as pools. But, many state regulators expect to see support for all adjustments in your work files.

We all need a Book of Adjustments ;>

Of course, all of us have adjustments that we have accumulated over the years, or recently developed. But, with CU we are being compared to peer and model adjustments. Of course, no one tells us who or what they are. Sometimes appraisers are given this information.

Regression to support adjustments

Regression will not work for all adjustments. It works well in conforming tracts less than 10 years old. After that, it goes downhill. This has been shown many times for AVMs. I really wish I could just buy regression software and have it calculate them all for me!!

Using qualitative adjustments

I did my first SFR appraisals this week without not making any dollar adjustments when I use form reports for non-lending work. I did make time adjustments (which are very easy to support) as the effective date was June, 2014, when prices were increasing rapidly in my market.

I used plus and minus signs in the grid. I use the 2005 Fannie forms but do not use the Fannie certification or limiting conditions. I use my own.

For awhile in the late 80s or early 90s Fannie had a form with pluses and minuses, so I had some experience. Also I don’t use dollar adjustments in my 5+ unit apartments or commercial appraisals.