The Most Unusual Homes Available Right Now, for sale or for rent, From A Luxury Cave To A Giant Turtle

Excerpt:

Good investment or not, wacky homes sure are fun to look at and can be rewarding to owners in ways more profound than money (more on that below). So we went in search of some of the most interesting homes available today. We found a house shaped like an onion, an Irish castle and a home meant to look like a fishing reel.

My comment: Just For Fun!! I wanna rent one of the vacation rentals. The Turtle House in Egypt is only $54 to $96 per night!! And you thought some of the weirdo homes you appraised were strange… take a look at these! And, of course, Ace Appraiser Jonathan Miller is mentioned in the first paragraph ;>

http://www.forbes.com/sites/samanthasharf/2016/09/23/from-gold-mines-to-torpedo-testing-plants-the-most-unusual-homes-available-right-now/

—————————

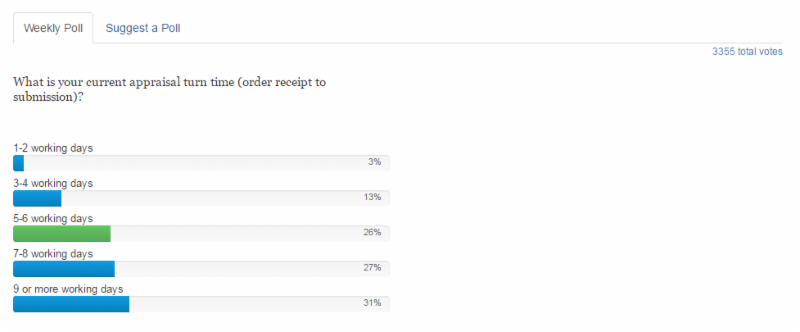

What is your current appraisal turn time (order receipt to submission)?

www.appraisalport.com poll

My comment: I wonder how many are over 2 weeks? 8 weeks?

WHAT DO YOU THINK? POST YOUR COMMENTS AT www.appraisaltodayblog.com !!

—————————

Viginia Coalition of Appraiser Professionals (VaCap) Open Letter to AMCs

A few weeks ago, Virginia Coalition of Appraiser Professionals (VaCAP) sent out an open letter to the AMCs. This letter was republished by many coalitions, and appraiser groups across the country; liked and shared on Facebook and broadcast on several industry blogs. VaCAP received an overwhelmingly positive response from the letter. We even heard from several Realtors applauding our efforts! Activity is still ongoing with comments! Click here to read the letter and comments!

We heard you loud and clear…

The letter can now be signed by individual appraiser here on AppraisersBlogs. We will gather signatures and submit the signed letter to the FDIC, CFPB, Comptroller of the Currency and our Federal Reserve Board.

Note: To protect the appraiser identity from retaliation, only the initial of your last name and state will show on line. The copies sent to the FDIC, CFPB, Comptroller of the Currency and our Federal Reserve Board will have your full name.

Excerpt of a few points on the list:

- – The use of an AMC has decreased the income of the appraiser, thereby harming local economies.

- – The use of an AMC has increased the turn time for the delivery of the appraisal.

- – AMCs operate on a fast and cheap model which has deteriorated the quality of appraisals

- – AMCs have caused undue stress on the appraiser by demanding constant updates

- – AMCs hire unqualified employees that lack comprehension of the appraisal process.

My comment: I usually don’t put in links to negative blog posts, but this seems to hit all the AMC issues, plus has something you can do. AMCs have been around since the 1960s but were never like this before. It is definitely a Big Mess and bad for the consumer (higher appraisal fees, delays in getting loans, etc.) Of course, they are doing what their lender clients want, but their methods are not good. There are some AMCs that are okay. Some appraisers have found a few they work for. Note: There is an ad in the middle of the post.

http://appraisersblogs.com/appraisers-sign-vacap-amc-letter/

——————————

In the October 2016 issue of Appraisal Today

Fees are going way up!! How to get higher appraisal fees during this boom time!! By Ann O’Rourke, MAI, SRA, PDQ and Doug Smith, SRA, AI-RRS . Lots and lots of practical tips.

Excerpt from the article:

How many appraisers are raising their fees?

I have been telling appraisers to raise their fees since early 2015. Below are two results of

appraisalport weekly polls.

Results from an April 2015 AppraisalPort weekly poll

Question: How long has it been since the last time you actually raised your fees?

- 1 year 17%

- 2-3 years 18%

- 4-6 years 18%

- 7+ years 26%

- I can’t remember – I normally just accept the fee my client offers. 21%

Back in April 2015 not many appraisers were raising their fees.

In the past year, have your standard fees for a typical non-complex assignment changed?

Results from Appraisalport September 2016 poll.

- Decreased 3

- Stayed about the same 42

- Increased by less than $50 27%

- Increased by less than $100 18%

- Increased by more than $100 11%

More appraisers are raising their fees in 9/16, but 45% have not still raised their fees! A few years ago I raised my non-lender fees to close to what borrowers pay. Why do appraisers keep working for low fees when they are so busy that they can’t take any more work? Or, they are not super busy, but want to get higher fees? Fear of never getting any more work. This is common to almost every business person, including myself. But it is not good when it keeps you from making more money, as it always does.

To read the full article with lots more data and practical tips for getting higher fees, plus 2+ years of previous issues, subscribe to the paid Appraisal Today.

$8.25 per month, $24.75 per quarter, $89 per year (Best Buy)

or $99 per year or $169 for two years

Subscribers get, FREE: past 18+ months of past newsletters

plus 4 Special Reports, plus 2 Appraiser Marketing Books!!

To purchase the paid Appraisal Today newsletter go to

————————————————–

17 Things Appraisers Should Do Before Hiring an AMC Client

October 4th, 2016 9:54 AM

Here are two of them:

7. Google the AMC’s name and see what comes up. This might seem obvious, but some AMCs have been in the news for lawsuits related to unfavorable treatment of appraisers. You do not want to waste your time vetting an AMC that has a bad reputation. Even if no lawsuits come up, a quick Google search could result in a feel for the company and let you know if this is a company you want to work for. Remember that homeowners might think you work for this AMC when you show up to do the appraisal. Is this a company that you are okay with if homeowners get confused and think you work for them?

17. Check the AMC’s data protection policy and ask what steps have been taken to keep your private information safe. Also ask if the AMC has ever had any data breaches and if so, determine what systems have been put into place to ensure that data breaches do not happen again. Does the AMC have a policy that requires them to alert appraisers if they believe a data breach was possible?

Click here for the full Most Excellent List!!

www.aqualityappraisal.com.blog

——————————————–

AMC Notes from Appraiserville by Jonathan Miller

Excerpts:

There was a CNBC article this week by Diana Olick that caused an uproar in the appraisal industry: ‘Massive’ shortage of appraisers causing home sales delays. Besides the incorrect inference of the title, the article was centered around Brian Coester, CEO of the Maryland-based CoesterVMS, currently one of the most controversial personalities in the appraisal management industry…

So I spoke with Diana Olick about the article this morning. I’ve known her for a long time and read all her stuff. She clearly did not realize what CoesterVMS represents to the appraisal industry but learned this from the outpouring of negative comments on the article by outraged appraisers. She understands now. How great is it that appraisers are getting out there and speaking their mind!

I told her that Coester is a notorious AMC in the middle of a big lawsuit that the entire appraisal industry is following. The shortage of appraisers is a myth being perpetuated by AMCS like Coester since their model only works if they pay appraisers a third to half the market rate for appraisal services.

My comment: I definitely think the current AMC model is broken, from the consumer, lender, appraisal and appraiser sides. I don’t really understand how it got so bad. I started writing in my paid newsletter about AMCs in the early 1990s. AMCs started in the were never like this before. Mostly they just paid lower fees. None had really low fees, scope creep, harassing and demeaning appraisers, etc.

To read more, Scroll down the page to Appraiserville

http://www.millersamuel.com/note/september-30-2016

—————————-

Miller was on a recent Voice of Appraisal radio interview with Phil Crawford.

Miller’s interview starts at -25:09 or 17:20 (download) 43:31 minutes total

http://www.voiceofappraisal.com/podcasts Episode 123

My comment: In last week’s email newsletter I said that the 2016 peak is almost up to the 2013 peak. In 2013 no one was complaining about high fees and turn times. In their discussion Miller said it was different because of CU/Scope Creep. He also said that business had been very slow between 2008 and 2012 and appraisers were glad for work. Appraiser attitudes about working for AMCs is much, much worse now. Good comments…Very few appraiser complaints about direct lenders and non-lender work.

————————————

Revised FHA handbook

Thanks to Dave Towne for this info!

HUD/FHA recently updated and revised the 4000.1 Handbook…..actually on June 30, 2016………..but notice about this was sent out Friday, Sept. 30.

http://portal.hud.gov/hudportal/HUD?src=/program_offices/housing/sfh/handbook_4000-1

When the page opens, scroll down the page and you’ll see two entries on the left regarding the Handbook. If you open the PDF link, and let it load…it will actually show you the changes made to the appraisal section (and others).

Note….the handbook is 1000+ pages, but only about 40 or so apply to appraisals.

Note that the revised handbook has ‘moved’ the Appraiser and Property Requirements section to II D, from its former position in B.

Buried in the revision is new info on how to account for specific named ‘appliances’ in a home you are appraising. See II D 3e.

It’s going to take someone with more time (than I have now) and expertise to determine what exactly HUD changed in the reporting requirements about “appliances that remain and contribute to value.” One needs to read the former 4000.1 Handbook and compare that to this revised edition to fully understand the implications of what HUD wants reported.

You will want to compare the attic observation requirement also. Revision 4000.1 has this in II D 3k.

Crawl space observation is in II D 3m.

————————————————-

HOW TO USE THE NUMBERS BELOW. Appraisals are ordered after the loan application. These numbers tell you the future for the next few weeks. For more information on how they are compiled, go to https://www.mba.org

Note: I publish a graph of this data every month in my printed newsletter, Appraisal Today. For more information or get a FREE sample issue go to www.appraisaltoday.com/productsor send an email to info@appraisaltoday.com . Or call 800-839-0227, MTW 8AM to noon, Pacific time.

WASHINGTON, D.C. (October 5, 2016)

Mortgage applications increased 2.9 percent from one week earlier

according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending September 30, 2016.

The Market Composite Index, a measure of mortgage loan application volume, increased 2.9 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 3 percent compared with the previous week. The Refinance Index increased 5 percent from the previous week. The seasonally adjusted Purchase Index decreased 0.1 percent from one week earlier. The unadjusted Purchase Index decreased 0.2 percent compared with the previous week and was 14 percent lower than the same week one year ago.

The refinance share of mortgage activity increased to 63.8 percent of total applications from 62.7 percent the previous week. The adjustable-rate mortgage (ARM) share of activity increased to 4.5 percent of total applications.

The FHA share of total applications decreased to 10.0 percent from 10.2 percent the week prior. The VA share of total applications decreased to 11.4 percent from 11.9 percent the week prior. The USDA share of total applications increased to 0.7 percent from 0.6 percent the week prior.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($417,000 or less) decreased to 3.62 percent, the lowest level since July 2016, from 3.66 percent, with points decreasing to 0.32 from 0.33 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans. The effective rate decreased from last week.

The average contract interest rate for 30-year fixed-rate mortgages with jumbo loan balances (greater than $417,000) decreased to 3.60 percent from 3.64 percent, with points decreasing to 0.25 from 0.28 (including the origination fee) for 80 percent LTV loans. The effective rate decreased from last week.

The average contract interest rate for 30-year fixed-rate mortgages backed by the FHA decreased to 3.50 percent from 3.52 percent, with points decreasing to 0.16 from 0.21 (including the origination fee) for 80 percent LTV loans. The effective rate decreased from last week.

The average contract interest rate for 15-year fixed-rate mortgages decreased to 2.93 percent from 2.95 percent, with points decreasing to 0.32 from 0.38 (including the origination fee) for 80 percent LTV loans. The effective rate decreased from last week.

The average contract interest rate for 5/1 ARMs remained unchanged at 2.92 percent, with points increasing to 0.44 from 0.40 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The survey covers over 75 percent of all U.S. retail residential mortgage applications, and has been conducted weekly since 1990. Respondents include mortgage bankers, commercial banks and thrifts. Base period and value for all indexes is March 16, 1990=100.

——————————————————————–

——————————————————————–