Not much interesting newz this week, so I’m sending some interesting links, sorta appraiser-related – use of “they”, cul-de sacs, street grids and the history of screws;>

Debunking the Cul-de-Sac

The design of America’s suburbs has actually made our streets more dangerous

Excerpt: Descend from 40,000 feet into just about any major metropolitan airport in the United States, and patterns of the trajectory of American life over the last century become clearly visible. Old urban cores are etched out in tight grids modeled off a sheet of graph paper. Further out, all those neat lines and right angles begin their curling meander into suburbia. Sparsely populated roads loop through the countryside in an odd geometry designed around the residential real estate dream of post-war America: a cul-de-sac for every family.

This is where it’s most apparent – from an airplane window – that American ideas about how to live and build communities have changed dramatically over time. For decades, families fled the dense urban grid for newer types of neighborhoods that felt safer, more private, even pastoral. Through their research, Garrick and colleague Wesley Marshall are now making the argument that we got it all wrong: We’ve really been designing communities that make us drive more, make us less safe, keep us disconnected from one another, and that may even make us less healthy.

http://www.citylab.com/design/2011/09/street-grids/124/

My comment: younger people are definitely not doing as much driving, and fewer are getting driver’s licenses, as in the past. I got my driver’s license at 15 ½ like everyone else. The baby boomers are getting older. Suburbia requires having a car. What if you don’t want to drive at night, or don’t want to drive much any more? As an appraiser I used to drive a lot. Now I just don’t want to drive for many hours a day. Of course, there is a lot of traffic now that the recession is behind us and everyone is driving again.

——————————

The Linguistic Turf Wars Over the Singular ‘They’

It could be close to mainstream acceptance.

Excerpt: Of all the turf wars that have complicated the landscape of grammar over the past few hundred years, the most complicated and frustrating may be that of the singular they.

It may be the most controversial word use in the English language-because it highlights a hole where a better-fitting word should go.

It creates a conflict between writers and editors who want things to follow the natural symmetry of Latin, and people who find they the only logical option for referring to a single person without a gender attached.

My comment: Almost everyone who writes anything, including emails, comes across this issue. I do. I have started using they more often, but did not know it was a new trend.

http://www.atlasobscura.com/articles/the-linguistic-turf-wars-over-the-singular-they

————————————-

The Screw Heads That Tried, But Failed, to Topple Phillips

The history of the screw is long and surprisingly weird.

Excerpt: The screw is the ultimate example of an object that hides under our noses but we never think about.

It’s the most basic of building blocks, something that connects every one of our devices, manufacturing processes, and likely even the chair you’re sitting in right now. (One device that doesn’t tend to have screws? The air mattress.)

And generally, we never give screws a second thought. But I was thinking about them a lot the other night when I tried to screw a nut around a screw and misaligned it so annoyingly that it took a lot of physical might to unscrew that screw.

Where do screws come from? And what did we do in a world before them? As it turns out, screws have a surprisingly diverse and unexpected history, stretching from ancient Greece to what we think of them as today, essential parts of our literal foundations. In ancient Greece, for example, it’s claimed Archytas of Tarentum invented an early version. Leonardo da Vinci also had one, and, later, of course, it was a key part of the Industrial Revolution.

My comment: Very Interesting, as Usual…

http://www.atlasobscura.com/articles/the-screw-heads-that-tried-but-failed-to-topple-phillip

———————————————

In the October 2016 issue of Appraisal Today

- Fees are going way up!! How to get higher appraisal fees during this boom time!! By Ann O’Rourke, MAI, SRA, PDQ and Doug Smith, SRA, AI-RRS . Lots and lots of practical tips. No one knows when the inevitable crash will come. My fees have gone way up.

- Pro Camera 9 – a great photo app for appraisers – only $4.99!! by Wayne Pugh, MAI, SRA – I want it and Love the price…

- USPAP 2017-2019 2nd Exposure Draft – what has changed? Comments due by October 14!! Tell the ASB what you think. Draft reports (again). They keep trying…. And extraordinary assumption and sales history plus some less interesting topics (to me)

An excerpt from Advisory Opinion 37, Computer Assisted Valuation Tools:

Q: An appraiser used a regression analysis model that suggests a relationship between the size of a residence and the price per square foot of similar residences in a specific market. This relationship has not been confirmed by the actions of market participants. Can the appraiser use the regression analysis as support for the GLA adjustment in the appraisal?

A: No, because the appraiser does not know how 1the regression analysis model works, has not independently tested the conclusions it provides, and has no reason to believe the database is reliable.

Another Q: An appraiser has purchased a software package that has multiple functions, such as market analysis, deriving adjustments for physical characteristics, automatically inputting information from the local MLS, and more.

He uses the program to develop an adjustment for an in-ground pool.

A. No… (They could have used “they” instead of “him”. See above on linguistics and using “they”.)

To read the articles, plus 2+ years of previous issues, subscribe to the paid Appraisal Today

$8.25 per month, $24.75 per quarter, $89 per year (Best Buy)

or $99 per year or $169 for two years

Subscribers get, FREE: past 18+ months of past newsletters

plus 4 Special Reports, plus 2 Appraiser Marketing Books!!

To purchase the paid Appraisal Today newsletter go to

If you are a paid subscriber and did not get the September 2016 issue, emailed September 1, 2016, please send an email to info@appraisaltoday.com and we will send it to you!! Or, hit the reply button. Be sure to put in a comment requesting it ;>

———————————————————-

UAD absolute vs relative

Another good commentary from Washington appraiser Dave Towne!!

Why is it so many appraisers have trouble with UAD and the CU (Collateral Underwriter), and how to apply the Quality and Condition rating between the Subject and Comps?

Not long after the UAD was implemented/mandated by FNMA (in 2011), and then the CU evaluation system came along, FNMA began discovering that many appraisers were improperly Rating the comps Quality and Condition AGAINST the Subject in the grid. And they began telling appraisers what they were finding. FNMA also discovered, and revealed, that many appraisers were using the same Comps over and over again in different reports, but were using DIFFERENT rating ‘numbers’ for those properties – depending on the Quality and Condition they applied to the SUBJECT.

Applying an ‘opinion’ of the difference for the Quality and Condition is not how we are supposed to do appraisals. Although many appraisers were taught to do that years ago by their mentors, who were also doing it wrong. Unfortunately, FNMA never really said much about it then….until the CU process started. So bad habits started, and were transferred from one appraiser to another, and down the line.

Everything on the grid pages is ABSOLUTE to those properties. The Address, the Site size, View, Design, Actual Age, GLA size, Garage & Carport spaces, etc. Everything. As I like to say – “It is what it is, where it is, when it is.”

Yet many appraisers still think the Rating for Quality and Condition for Comps should be applied Relative-to the Subject. Uh….NO! The Comps are rated what they are, based on the Quality and Condition Rating Definitions that apply with UAD. (And so is the Subject.)

Over the years, I’ve read countless laments by appraisers who say the ‘UAD definitions’ are hard to understand, and don’t have ‘steps’ between the numbers so appraisers can try to engineer precise differences in the ratings and resulting adjustments. That line of thinking is basically hogwash. (If you think you need to make more precise adjustments, you can do so on the extra grid lines…such as ‘Add’l Qual Adj.’ or the same for Cond.

Why do I believe this is so? Let me ask you who believe UAD definitions are so difficult: Before UAD came along, did you ever include definitions of the ‘rating words’ we used back in the dark ages – in your reports? That can be answered 100% no (except by some very elite appraisers). Another question: Where did those ‘rating words’ come from, and can you quickly pull out your reference guide to bring up the definitions for those?. Again, probably 100% no. Before you whine, send me your definitions of Average(+) and Excellent(-), for both Quality and Condition – that you used prior to UAD.

So now we have UAD and the basically easy to use and understand definitions. These, by the way, should be included in every appraisal report – all the software vendors have definition pages to add into reports. Not including these in reports means you have produced a report that is NOT CREDIBLE per USPAP because without those, the reader(s) won’t know what the rating numbers and other codes mean.

Be sure to check out the many comments at:

http://appraisersblogs.com/UAD-rating-absolute-vs-relative

My comment: I thought this had been figured out by most appraisers many years ago. But, change can be difficult, especially something you have been doing for many years .Of course, if you don’t do work requiring UAD, you can do what you have always done – relative. I love relative!!

————————

What Your Street Grid Reveals About Your City

The surprising ways size and shape can impact a place’s economic productivity and walkability.

Excerpts: New York, of course, is not the only city built on a grid. Similar schemes could be found as far back as ancient Greece and Rome. But Manhattan’s design was the exemplar for what became the default pattern of American cities.

Still, not all grids are created equal. Some shape a walking-friendly streetscape. Others, not so much. Over at the Strong Towns blog, Andrew Price, a software developer by day who blogs about urbanism, has been writing about the math of the grid and what it reveals about a city’s economic productivity and walkability.

My comment: Very interesting article on street grids: math, different layouts, what the patterns mean…

http://www.citylab.com/commute/2013/12/what-your-street-grid-reveals-about-your-city/7746/

———————————————————

Nonbank Lenders’ Market Share is at a Two-Decade High. Here’s Why

Excerpt: Depositories still dominate home lending, but nondepositories’ market share is the highest it has been in at least two decades.

The nonbank share of total mortgage originations was 42% in 2014, according to an analysis of Home Mortgage Disclosure Act data by ComplianceTech and its LendingPatterns.com tool. Just five years before that, in 2010, nonbanks held only a 27% market share.

One reason for this is that banks’ attraction to mortgages tends to be opportunistic.

“Banks have historically been very fickle about the mortgage lending market,” said Maurice Jordain-Earl, managing director and co-founder of ComplianceTech.

http://www.nationalmortgagenews.com/news/origination/nonbank-lenders-market-share-is-at-a-two-decade-high-heres-why-1086192-1.html

My comment: Ever heard of Quicken Loans? My loan is with them. Lots of appraisers work for their AMC. For appraisers, this means fewer lenders that don’t use AMCs. The non-banks use AMCs.

——————-

Another interesting article on non banks: Why Nonbank Lenders Are the Future of Mortgages

http://www.nationalmortgagenews.com/news/voices/why-nonbank-lenders-are-the-future-of-mortgages-1072042-1.html

——————————–

In San Francisco, a Tilting Skyscraper and a Deepening Dispute

Excerpts:

SAN FRANCISCO – The developers of the luxurious Millennium Tower laid out the risks and potential defects of the 58-story building in minute detail when its apartments went on sale seven years ago.

The Milennium Tower, which its developers say is the largest reinforced concrete building in the western United States, has now sunk about 16 inches and is leaning six inches toward a neighboring skyscraper.

The color and texture of the marble and granite hallways “may not be completely uniform,” said a disclosure statement given to potential buyers. The streets below the tower could be “congested and noisy,” and the landscaping in the common areas could change, subject to availability of certain species of plants.

But the 21-page disclosure document left out what owners of units in the buildings now say was a crucial detail: that the building had already sunk more than eight inches into the soft soil by the time it was completed in 2009, much more than engineers had anticipated.

http://www.nytimes.com/2016/09/23/us/san-francisco-millennium-tower-dispute.html

————————————————-

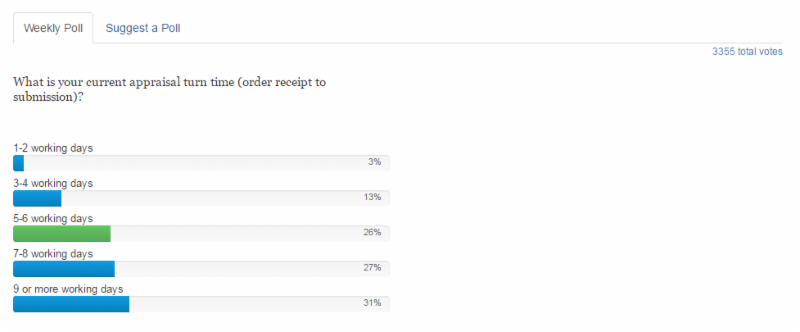

I just finished my mortgage application volume graph from 1/13 to 9/16 for my paid newsletter. For the first time, it was close to the peak in early 2013 a few weeks ago. That’s why appraisers are so busy. But, why are there so many complaints about high fees and long turn times now? Is is just media hype? Or have more appraisers quit working for AMCs???

HOW TO USE THE NUMBERS BELOW. Appraisals are ordered after the loan application. These numbers tell you the future for the next few weeks. For more information on how they are compiled, go to https://www.mba.org

Note: I publish a graph of this data every month in my printed newsletter, Appraisal Today. For more information or get a FREE sample issue go to www.appraisaltoday.com/products or send an email to info@appraisaltoday.com . Or call 800-839-0227, MTW 8AM to noon, Pacific time.

WASHINGTON, D.C. (September 28, 2016) – – Mortgage applications decreased 0.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending September 23, 2016.

The Market Composite Index, a measure of mortgage loan application volume, decreased 0.7 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 1 percent compared with the previous week. The Refinance Index decreased 2 percent from the previous week. The seasonally adjusted Purchase Index increased 1 percent from one week earlier. The unadjusted Purchase Index remained unchanged from the previous week and was 10 percent higher than the same week one year ago.

The refinance share of mortgage activity decreased to 62.7 percent of total applications from 63.1 percent the previous week. The adjustable-rate mortgage (ARM) share of activity remained unchanged at 4.4 percent of total applications.

The FHA share of total applications remained unchanged at 10.2 percent from the week prior. The VA share of total applications increased to 11.9 percent from 11.6 percent the week prior. The USDA share of total applications decreased to 0.6 percent from 0.7 percent the week prior.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($417,000 or less) decreased to 3.66 percent from 3.70 percent, with points decreasing to 0.33 from 0.38 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans. The effective rate decreased from last week.

The average contract interest rate for 30-year fixed-rate mortgages with jumbo loan balances (greater than $417,000) decreased to 3.64 percent from 3.69 percent, with points decreasing to 0.28 from 0.29 (including the origination fee) for 80 percent LTV loans. The effective rate decreased from last week.

The average contract interest rate for 30-year fixed-rate mortgages backed by the FHA decreased to 3.52 percent from 3.56 percent, with points decreasing to 0.21 from 0.23 (including the origination fee) for 80 percent LTV loans. The effective rate decreased from last week.

The average contract interest rate for 15-year fixed-rate mortgages decreased to 2.95 percent from 2.99 percent, with points increasing to 0.38 from 0.35 (including the origination fee) for 80 percent LTV loans. The effective rate decreased from last week.

The average contract interest rate for 5/1 ARMs decreased to 2.92 percent from 2.96 percent, with points increasing to 0.40 from 0.26 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The survey covers over 75 percent of all U.S. retail residential mortgage applications, and has been conducted weekly since 1990. Respondents include mortgage bankers, commercial banks and thrifts. Base period and value for all indexes is March 16, 1990=100.