A Map of the Last Remaining Flying Saucer Homes

All the 1960s Futuro Houses left in the world.

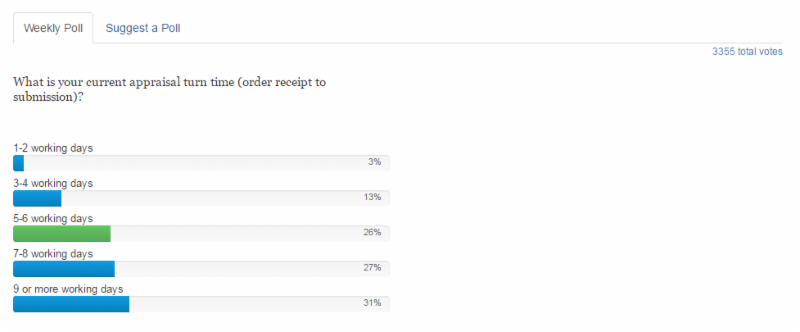

Just For Fun!! Take a break from writing up those darn appraisal reports ;>

Excerpt: The Futuro House, in all its space age retro splendor, is like a physical manifestation of 1960s optimism. Shaped like the Hollywood idea of a flying saucer, the Futuro is a plastic, prefabricated, portable vacation home built to easily adapt to any climate or terrain, from mountain slopes to the seaside. After enjoying a heyday in the late ’60s and early ’70s, the remaining Futuros are now scattered across all parts of the globe, from the Australian beaches to the mountains of Russia, like secluded relics of midcentury technoutopianism.

Very interesting!!

http://www.atlasobscura.com/articles/a-map-of-the-last-remaining-flying-saucer-homes

My comment: I love atlasobscura.com. The strange homes and buildings I include in these emails are just the tip of the iceberg!!!!

——————

What is your typical rush fee?

www.appraisalport.com poll.

My comment: Rush fees are another way to make more money during this boom time, to save for the downturn when AMC fees will drop.

The most critical appraisals are those for purchases, which can require rush fees to get appraisers to drop their regular refi business and do them.

I am hearing about widely varying AMC fee increases from around the country, depending on the local market supply of appraisers willing to work for AMCs I guess. Savvy AMC appraisers reply to low bids with an increased fee. After a few weeks, sometimes their fee is accepted. Local appraisers I know only work for a very few select AMCs, if any. But, when business slows way down, they take more AMC work. I also hear from appraisers in the same market with widely varying fees that they will accept.

What do I do? Rush fees stress me out too much as I am very backed up. I just put new appraisal requests in my queue, which is typically around 60 days. Sometimes I will do one faster if it is a special circumstance and/or a referral from a local real estate agent, but I don’t require a rush fee. When I used to do appraisals for purchases, I always gave them priority but never charged a rush fee. I am definitely in the minority!!

What do you think? Post your comments at https://wp.me/p7jsxG-Cl !!!

——————————————

The Most Expensive House In The World Could Sell For $1.1 Billion

Just For Fun!! Take a break from writing up those darn appraisal reports ;>

Excerpt: What can justify a $1.1 billion price tag for a house?

Before searching for the features behind the number, let’s clarify that in this case, “the house” is rather a large, opulent mansion on the French Côte d’Azur, set in a “small” privileged refuge between Nice and Monaco frequently described as the ‘billionaires’ playground.’

First, there’s the house itself, with the understated name Villa Les Cèdres-The Cedars-at the center of Saint-Jean-Cap-Ferrat, known in French as a “presqu’île,” or “almost island.”

The description of the magnificent property in the French press includes 10 bedrooms, a ballroom, concierge, a chapel, 50-meter swimming pool dug into the rocks, a winter garden and stables for 30 horses.

My comment: I could take a few months (or more) to do an appraisal for a trip to France to appraise this property… Or maybe just an open house tour ;>

Very interesting!!

http://www.forbes.com/sites/ceciliarodriguez/2016/08/20/at-1-1-billion-the-most-expensive-house-in-the-world-in-france-goes-to-market

————————————

Beware of unknown desperate AMCs sending email solicitations

An appraiser I know, who only works for one AMC, received an email request from an AMC he had never heard of. He replied politely that he was not interested. He was added to their approved list and bombarded with requests for appraisals every day. It was a lot of hassle to get his name removed.

I seldom get any AMC appraisal requests by email or phone, or request to join their panel. I must be on a Do Not Call or Email List ;> I have been replying to emails saying I have never worked for an AMC. They are really getting desperate!! Now, I am thinking about not even replying.

==========================================

In the June 2016 issue of Appraisal Today

FHA attic inspection requirement

Excerpt: Inspection Tips – Insulation and attic access by Doug Smith, SRA, AI-RRS

When blown in insulation is added, the installer will often add an extension or dam to the scuttle that makes it difficult to fully observe the full attic.

Formerly, attics had walkways which when blown in insulation is applied, these walkways were covered with insulation. If the scuttle is in a closet and closet shelves make it difficult to fully access the attic, the difficulty with attic must be reported and a photograph taken to demonstrate the difficulty with attic access.

However, if the access is blocked by personal possessions, it may be practical to enlist the help of the homeowner to make the attic or scuttle accessible. In the instant case of the underwriter stating that a full inspection is required, the underwriter is incorrect.

The appraiser must document why a full inspection was not performed when there is not an accessible attic. Suggested language might include: “A full attic inspection was not

performed as the subject property does not have a readily accessible attic and only has scuttle access.” Along with a photo of what can be seen from the scuttle, the appraiser might add that the appraiser completed a head and shoulders inspection of the attic.

Remember to check the block on page one of the form that the attic is accessed by a scuttle. If the property has a full attic, note if a full inspection was performed and comment how access was gained either by stairway or drop stair.

To read the full article, plus 2+ years of previous issues, subscribe to the paid Appraisal Today.

$8.25 per month, $24.75 per quarter, $89 per year (Best Buy)

or $99 per year or $169 for two years

Subscribers get, FREE: past 18+ months of past newsletters

plus 4 Special Reports, plus 2 Appraiser Marketing Books!!

To purchase the paid Appraisal Today newsletter go to

If you are a paid subscriber and did not get the September 2016 issue, emailed September 1, 2016, please send an email to info@appraisaltoday.com and we will send it to you!! Or, hit the reply button. Be sure to put in a comment requesting it ;>

=====================================================

Selling a $5 Million, Seven-Story Basket Is No Picnic

Its size, location, and fundamental basket-ness make it tough to sell, even at a steep discount

Thanks (again) to Jonathan Miller at http://www.millersamuel.com/housing-notes/

Excerpts: “You might see it three or four miles off before you come around the bend, and then you say, ‘That is a basket. That is unquestionably a basket,'” said Tom Rochon.

It is a basket, or rather, a seven-story office building shaped like one-a massive facsimile of the signature picnic basket made by the company once headquartered there. Some 40 miles outside Columbus, Ohio, the basket building, as it’s locally known, is one of the area’s grandest attractions, inviting quirky selfie-seekers, architecture nerds, and, of course, basket enthusiasts.

When the property – slightly larger than another Ohio landmark, Cleveland’s Rock and Roll Hall of Fame-was listed 18 months ago, the asking price was $7.5 million. Now it’s on the market for $5 million, or about $28 a square foot, about half of what traditionally shaped office buildings in the area usually sell for… commercial property in the area typically ranges from $50 to $80 a square foot.

The basket was built for about $32 million and finished in 1997.

http://www.bloomberg.com/news/articles/2016-09-07/selling-a-5-million-seven-story-basket-is-no-picnic

My comment: I regularly write about weird properties in my weekly emails, including the Basket House a few years ago. Finally we find out what it is (not) worth. Definitely an Appraisal Challenge!!

———————–

Status Quo Bias: ‘Linear” Thinking in the Real Estate Industry

by Jonathan Miller

Excerpt: When we look at forecasting, planning, trending or anything that includes a look out over the future, I find the real estate industry (i.e. appraisers, real estate agents & brokers) generally thinks along linear lines.

For example:

When housing prices rise…they will rise forever.

When housing prices fall…they will fall forever.

When sales activity rises…they will rise for ever.

When inventory falls…it will fall forever.

When rental prices rise…they will rise forever.

…and so on.

Where does this status quo bias come from?

Click here for some more interesting comments..

http://www.millersamuel.com/status-quo-bias-linear-thinking-in-the-real-estate-industry/

My comment: Of course, I completely agree. It is very important if you work in a market like mine, where residential prices seem to go from stable to increasing and back overnight. I have no idea why. I go on the broker open house tour every week and see what agents are saying. For example, only 1 or 2 offers vs. 5-6 and longer days on market

————————————————-

HOW TO USE THE NUMBERS BELOW. Appraisals are ordered after the loan application. These numbers tell you the future for the next few weeks. For more information on how they are compiled, go to https://www.mba.org

Note: I publish a graph of this data every month in my printed newsletter, Appraisal Today. For more information or get a FREE sample issue go to www.appraisaltoday.com/products or send an email to info@appraisaltoday.com . Or call 800-839-0227, MTW 8AM to noon, Pacific time.

WASHINGTON, D.C. (September 14, 2016

Mortgage applications increased 4.2 percent from one week earlier,

according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending September 9, 2016. This week’s results included an adjustment for the Labor Day holiday.

The Market Composite Index, a measure of mortgage loan application volume, increased 4.2 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 17 percent compared with the previous week. The Refinance Index increased 2 percent from the previous week. The seasonally adjusted Purchase Index increased 9 percent from one week earlier. The unadjusted Purchase Index decreased 15 percent compared with the previous week and was 8 percent higher than the same week one year ago.

The refinance share of mortgage activity decreased to 62.9 percent of total applications from 64.0 percent the previous week. The adjustable-rate mortgage (ARM) share of activity increased to 4.6 percent of total applications.

The FHA share of total applications increased to 9.6 percent from 9.5 percent the week prior. The VA share of total applications increased to 12.0 percent from 11.9 percent the week prior. The USDA share of total applications increased to 0.7 percent from 0.6 percent the week prior.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($417,000 or less) decreased to 3.67 percent from 3.68 percent, with points decreasing to 0.36 from 0.37 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans. The effective rate decreased from last week.

The average contract interest rate for 30-year fixed-rate mortgages with jumbo loan balances (greater than $417,000) decreased to 3.64 percent from 3.66 percent, with points increasing to 0.36 from 0.30 (including the origination fee) for 80 percent LTV loans. The effective rate decreased from last week.

The average contract interest rate for 30-year fixed-rate mortgages backed by the FHA decreased to 3.50 percent from 3.52 percent, with points decreasing to 0.27 from 0.35 (including the origination fee) for 80 percent LTV loans. The effective rate decreased from last week.

The average contract interest rate for 15-year fixed-rate mortgages increased to 2.97 percent from 2.96 percent, with points unchanged at 0.34 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The average contract interest rate for 5/1 ARMs remained unchanged at 2.87 percent, with points increasing to 0.37 from 0.30 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The survey covers over 75 percent of all U.S. retail residential mortgage applications, and has been conducted weekly since 1990. Respondents include mortgage bankers, commercial banks and thrifts. Base period and value for all indexes is March 16, 1990=100.